Stores of Value: Part 4 - Alternative Diversifiers™

Building a more resilient defensive sleeve in a world of higher debt, persistent inflation risk and faster digitisation. Written by Jonas Benner and Stuart Eliot

12 minutes

“We all know what to do, but we don’t know how to get re-elected once we have done it.”

- Jean-Claude Juncker (former Prime Minister of Luxembourg and President of the European Commission)

In Parts 1 and 2 of this series, we explored gold and Bitcoin as stores of value and introduced a framework for thinking about assets whose primary purpose is to preserve purchasing power over time. In Part 3, we tested what adding gold and Bitcoin would have meant historically within a diversified portfolio, developed a forward-looking framework and discussed how investors might think about sizing such exposures.

In this fourth part, we take the portfolio question one step further. Rather than treating “defensive” as synonymous with “bonds”, we ask a practical question many advisers are now grappling with: if an investor is concerned about the long-run purchasing power of fiat currency, and is less confident that traditional fixed income will reliably diversify equity risk in the future, what should sit alongside (or partly in place of) bonds in a diversified portfolio?

Executive Summary

In this article, we propose a pragmatic answer2. With monetary debasement as a real risk, investors should build a defensive sleeve that is diversified in its diversifiers - blending complementary protections rather than relying on a single one.

We find that historical outcomes during crisis periods (and overall) are improved by replacing up to 20% of the portfolio allocation to bonds and cash within a ’70-30 style’ multi asset portfolio with a blend of long volatility, systematic alpha, and store of value assets.3

No single blend suits every investor, and each diversifier carries its own risks and costs (discussed later). With that caveat, a pragmatic replacement for bonds and cash might look like:

- 60% systematic alpha (which we model using the SG Trend Index4)

- 20% long volatility (modelled using the ‘Protection’ components of SouthPeak’s Alternative Alpha strategy5)

- 20% Store of Value assets (of which ~80% gold and 20% Bitcoin).

What we mean by monetary debasement (and why investors keep worrying about it)

Monetary debasement is a loaded term, so it is worth defining what we mean. In practice, most modern monetary systems are designed around a small, persistent rate of inflation. That design choice can be sensible because it helps economies adjust wages and prices, and it gives central banks room to cut rates in a downturn. But it also means the purchasing power of money is expected to decline over time. Debasement, in this sense, is simply the ongoing dilution of existing currency units through positive inflation targets, money and credit expansion, and (at times) fiscal pressures that encourage policy makers to prioritise near-term stability over long-term purchasing power.

There is nothing new about currency debasement. In Roman times under Augustus and the early Roman Empire the denarius, the standard silver coin of Rome was made of 95-98% silver. Within three centuries, the antoninianus, the successor to the denarius, had been so heavily debased that many contained less than 5% silver, often only as a thin surface coating. Henry VIII’s exploits included cutting the silver content in English coins from above 90% to below 25%. Spain brought so much silver back from the Americas (causing the money supply to explode) that prices rose six-fold over the next one and a half centuries.

The list goes on, including the 40% increase in US Money Supply in 2020-21. Let’s say that again: over that 2-year period, close to a third of all US money ever created came into existence which, we contend, resulted in the goods, services, and asset price inflation we continue to enjoy today.

One thing of which we can be confident, as illustrated by the opening quote, is that policymakers seeking re-election are not motivated to make tough choices and therefore in times of stress are more likely to ‘print’ money.

Whether one agrees with the framing or not, the key point for this article is behavioural and portfolio relevant. Investors periodically become more sceptical that “cash and bonds” will preserve purchasing power across cycles, especially when debt burdens are high and policy makers face difficult trade-offs. That scepticism tends to rise after inflation surprises, during periods of financial repression, or when real yields are low or negative. We are not trying to forecast near-term policy outcomes; we are instead highlighting the conditions under which the debasement concern tends to resurface and influence portfolio construction.

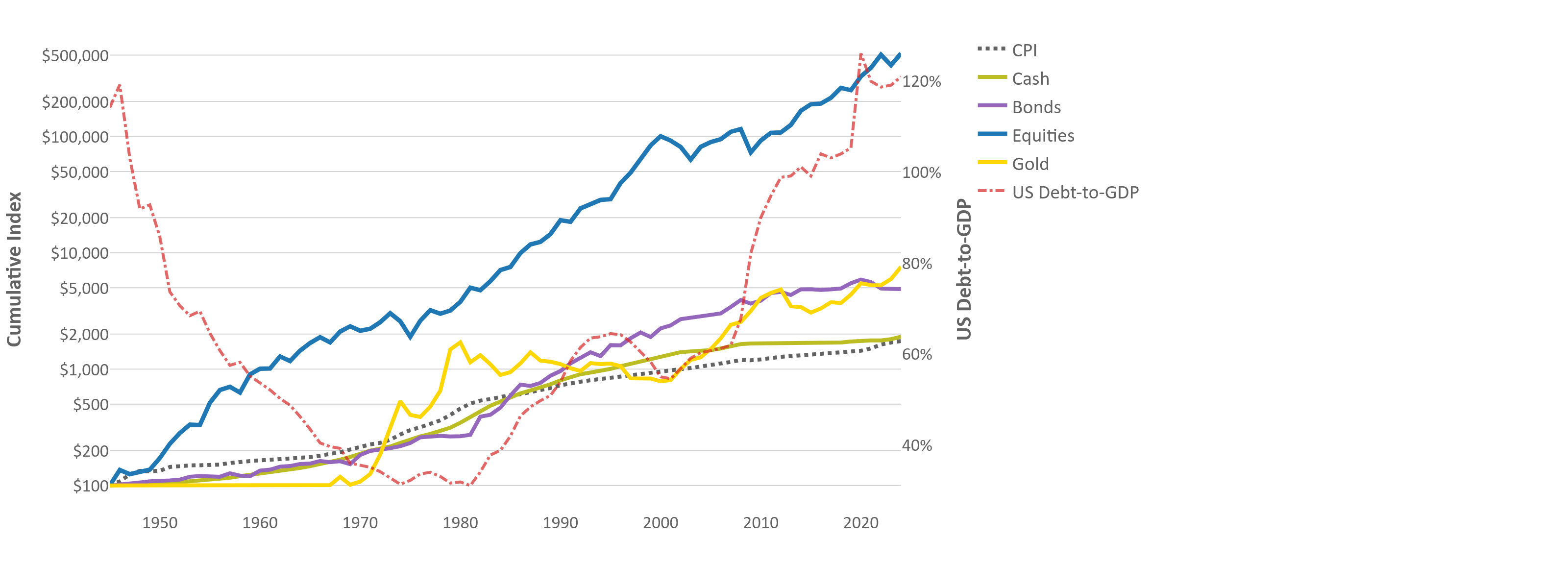

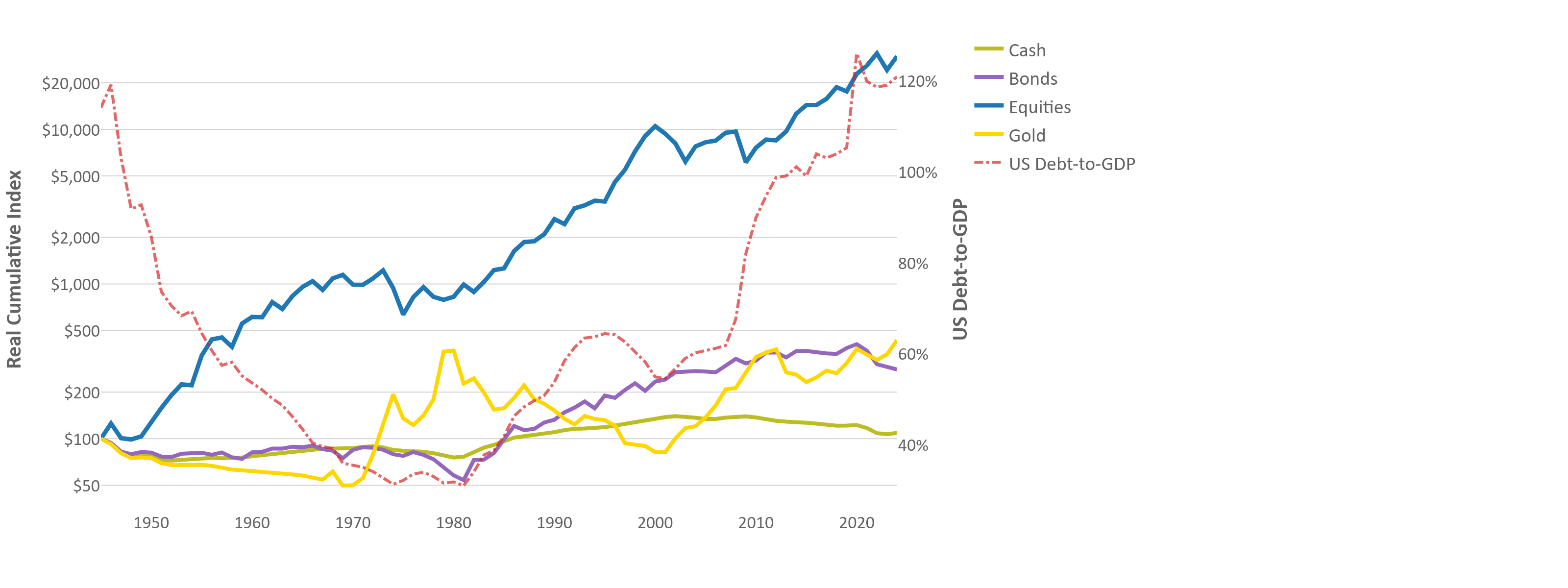

A useful starting point is to compare how major asset classes have behaved through long inflation and policy regimes. In the US from the mid-1940s onward, investors experienced multiple cycles where bonds were excellent diversifiers, and other cycles where bonds struggled to keep pace with inflation for long stretches. The lesson is that the reliability of a single defensive asset is regime-dependent. While this example is based on US data, we expect the insights to be relevant globally. The below charts show the cumulative US CPI and total returns for cash, bonds, equities, and gold since 1945, with US debt-to-GDP overlaid. The second chart deflates these returns by the CPI to convert them to real returns.

Cumulative US CPI & total returns for cash, bonds, equities and gold

Source: Federal Reserve Bank of Minneapolis, Bloomberg, Prof Robert Shiller

Cumulative US CPI & real (CPI-deflated) total returns for cash, bonds, equities and gold

Source: Federal Reserve Bank of Minneapolis, Bloomberg, Prof Robert Shiller

Looking at real (inflation-adjusted) cumulative returns shows that in some inflationary environments (mid-1940s until the 1980s), the real return of nominal bonds can be negative for years, even if they still play an important role as a crisis hedge. If an investor’s objective is to protect purchasing power over a full cycle, it is reasonable to ask what should complement traditional fixed income when inflation risk rises.

The portfolio design problem

The question we want to answer is straightforward: if you, as an investor or adviser, are concerned about the reliability of fixed income as the sole defensive anchor in a multi-asset portfolio, what complementary assets should you hold?

Part 3 showed that, historically, combining bonds with store of value assets improved diversification in several stress episodes. Here we extend that logic and suggest that rather than choosing one diversifier, investors should diversify across diversifiers - each designed to protect against a different kind of ‘bad outcome’.

Our answer: Alternative Diversifiers™

We call this sleeve Alternative Diversifiers™: a small set of liquid, repeatable exposures that are not primarily designed to maximise expected return, but to improve the distribution of outcomes for the overall portfolio, especially in severe drawdowns and inflationary regimes.

Conceptually, the sleeve combines four different types of protection:

- Gold: a long-standing store of value that has historically responded well to certain inflation and confidence shocks.

- Bitcoin: an emerging digital store of value with high uncertainty but meaningful asymmetric upside if adoption continues consistent with current trends.

- Long volatility / convexity: strategies designed to pay off in sharp risk-off events, providing explicit crash protection.

- Systematic alpha (low structural beta): trend-following, market-neutral, or low-beta strategies that seek persistent return premia without relying on broad equity beta.

These exposures are not substitutes for high-quality implementation, sensible sizing or good governance. They are building blocks that can be combined thoughtfully to reduce dependence on any single defensive asset.

Diversification of diversifiers: why multiple diversifiers work better than one

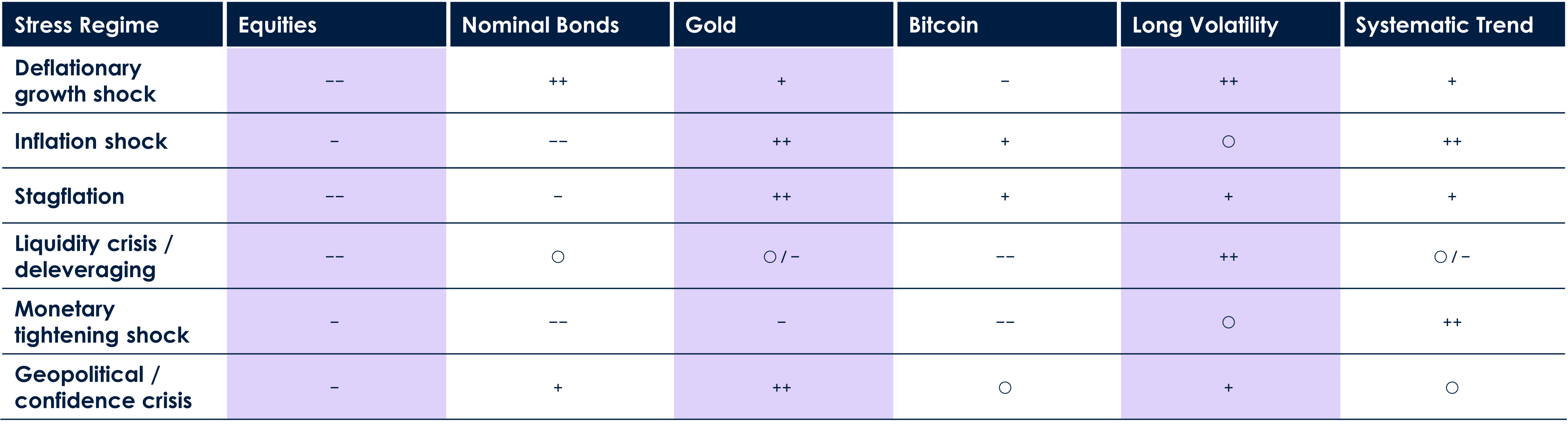

The core insight is that ‘crisis’ is not one regime. Portfolios can be hurt by very different forces: an inflation shock, a growth shock, a liquidity shock, a policy shock, or a confidence shock. Traditional bonds tend to work best in growth slowdowns and deflationary risk-off episodes. They can struggle when inflation is the dominant risk, or when term premia re-price sharply.

Regime Matrix: Expected Directional Behaviour Under Stress

Key: ++ strong positive, + positive, ○ neutral / ambiguous, − negative, −− strong negative. Source: AMP investments team

By combining diversifiers with different directional behaviours under stress, the portfolio’s shock response can become more robust. This will not eliminate drawdowns, but it is expected to reduce the severity of drawdowns coinciding with periods of high inflation and weak bond protection. Importantly, diversifying diversifiers reduces the risk of the diversifying asset sleeve losing value along with equities.

The diversifiers in detail

1) Gold

Gold has served as a store of value for millennia. In modern portfolios it has tended to perform best when investors are seeking safety from monetary disorder, negative real rates, or confidence shocks. It is liquid, widely held, and does not depend on the solvency of an issuer. Its weakness is that it can underperform for long periods in benign growth regimes.

2) Bitcoin

Bitcoin is still early in its monetisation process. Its risk profile is very different from gold: higher volatility, deeper drawdowns, and a stronger sensitivity to global liquidity conditions. But it also has unique properties, namely a fixed and transparent supply schedule, global portability, and the ability for holders to securely hold and verify the asset themselves. For some investors, a small allocation is best thought of as long-duration, asymmetric optionality on the adoption of a new monetary goodin a digital world.

3) Long volatility / convexity

Long volatility strategies aim to provide convex payoffs when markets experience sharp left-tail shocks. This can be implemented via options-based tail hedges, dynamic volatility strategies, or specialist managers that run systematic protection mandates. The trade-off is that explicit protection often has an ongoing cost (sometimes called ‘insurance bleed’) in calm markets. The design challenge is therefore twofold: (i) size the exposure so that the payoff is meaningful in a crisis, and (ii) manage the carry cost so the diversifier remains sustainable over a full cycle.

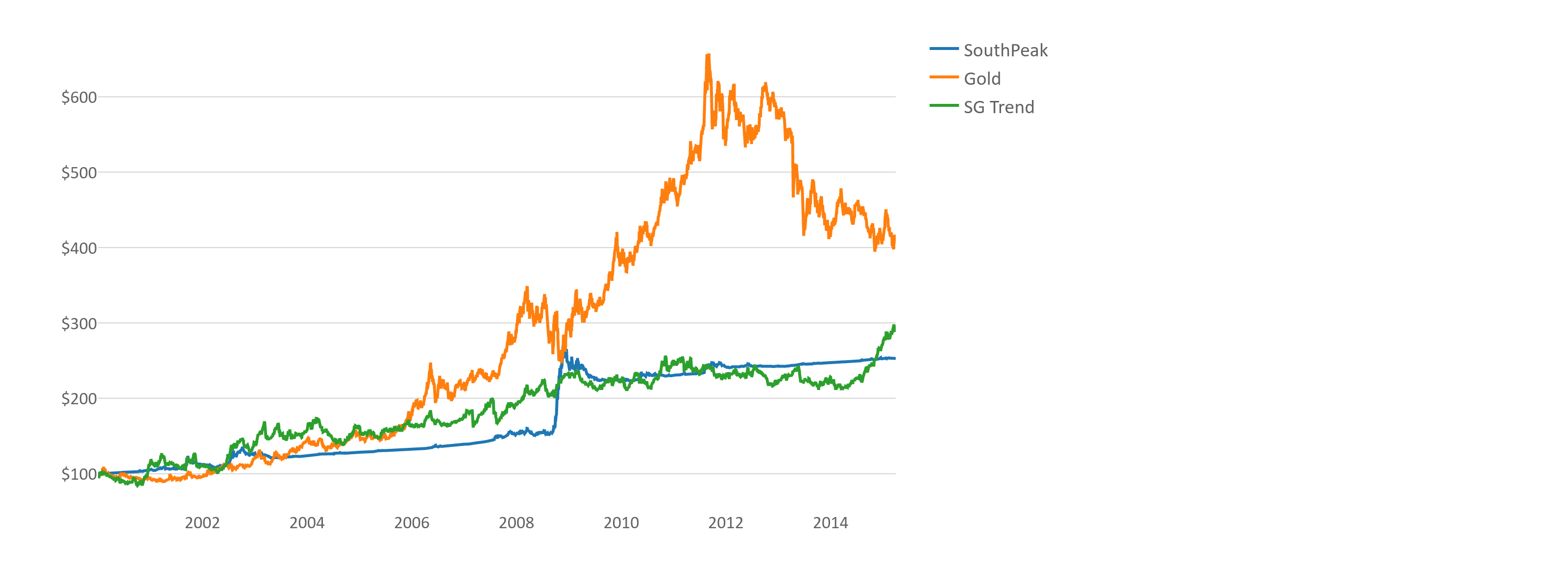

The return data we use for this component is the protection component of the SouthPeak Alternative Alpha Fund. We are grateful to SouthPeak for assisting with this project as long time series of long volatility returns are very hard to come by.

4) Systematic alpha with low structural beta

Systematic alpha refers to strategies that aim to generate returns from repeatable patterns or premia without taking a large, persistent exposure to broad market beta. Examples include trend following, market-neutral equity factors, statistical arbitrage, macro relative value, alternative risk premia, and certain forms of defensive carry strategies. These strategies can diversify event risk and liquidity risk because their return drivers are more dispersed than a single equity or duration exposure. They are not crisis hedges in the same way as long vol, but they can reduce reliance on equity beta for returns.

The return data we use for this component is the SG Trend Index. This index is constructed based on the actual returns of the largest multi-asset trend-following Commodity Trading Advisers (CTAs).

Implementation: sizing, rebalancing and practical guardrails

One way to implement Alternative Diversifiers™ is to fund them from a portion of the traditional defensive sleeve (bonds and cash), while keeping the growth sleeve (equities) unchanged. This keeps the portfolio’s long-run growth engine intact while improving the breadth of protection.

In the analysis that follows, we begin with a simple baseline implementation where Alternative Diversifiers™ are funded at 10%, 15% and 20% of total portfolio weight, taken pro-rata from the components of the defensive sleeve. Within the alternatives sleeve, we initially assume equal weights across the four components. This provides a transparent and easily understood starting point from which the broader logic of the sleeve can be assessed.

Later in the article we move from this baseline to more practical constructions that illustrate how investors might move from a simple conceptual implementation toward a more realistic practitioner-style portfolio.

Rebalancing matters. Store of value assets and convexity diversifiers can drift materially in strong trends or in sharp selloffs. A disciplined rebalancing policy (for example, monthly) helps keep risk within intended bounds and prevents one sleeve from dominating the portfolio.

Historical evidence: how would this have behaved?

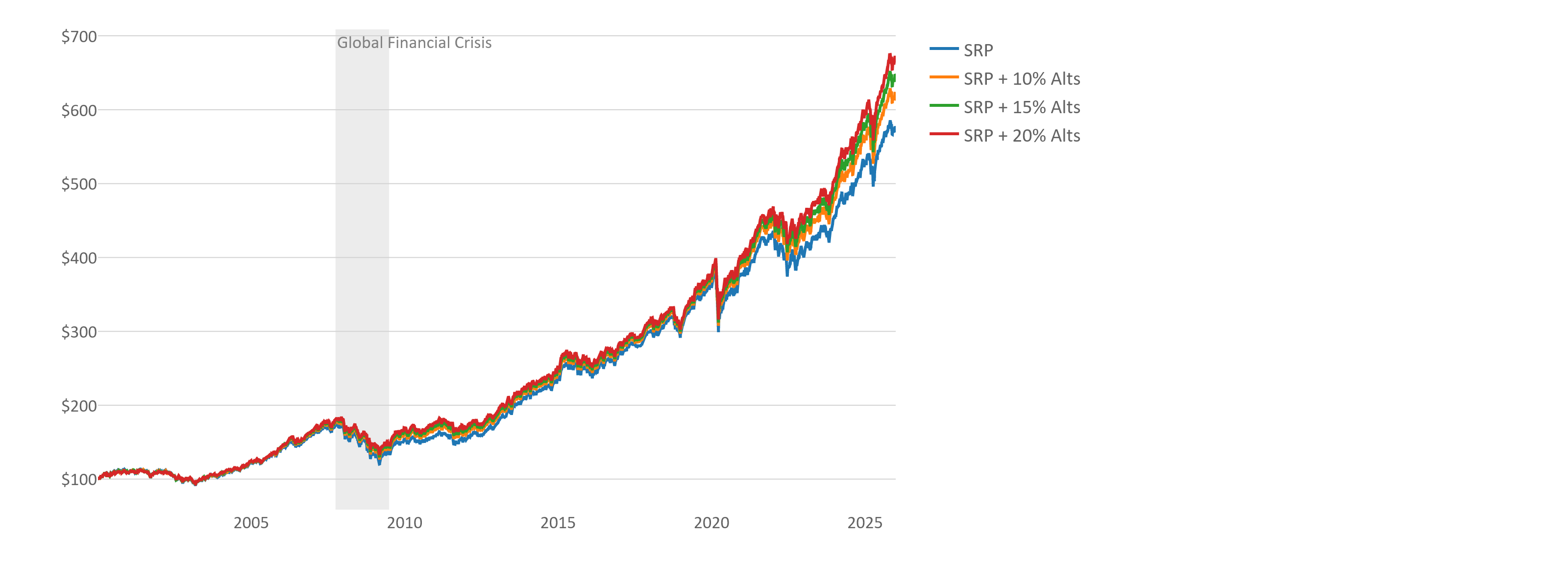

The intuition of Alternative Diversifiers™ is appealing, but portfolio construction must be grounded in data. We therefore test how a traditional diversified portfolio would have performed with incremental allocations to the Alternative Diversifiers™ sleeve, funded from the defensive sleeve.

Historical Performance (2015-2025)

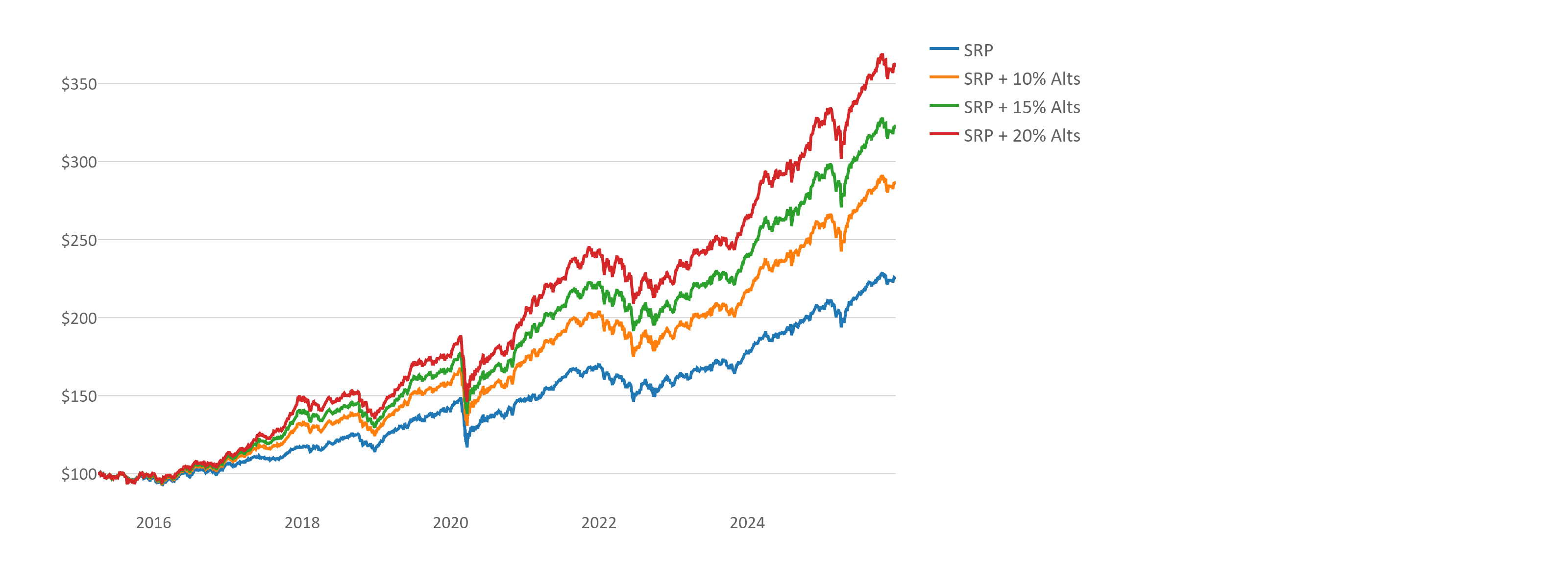

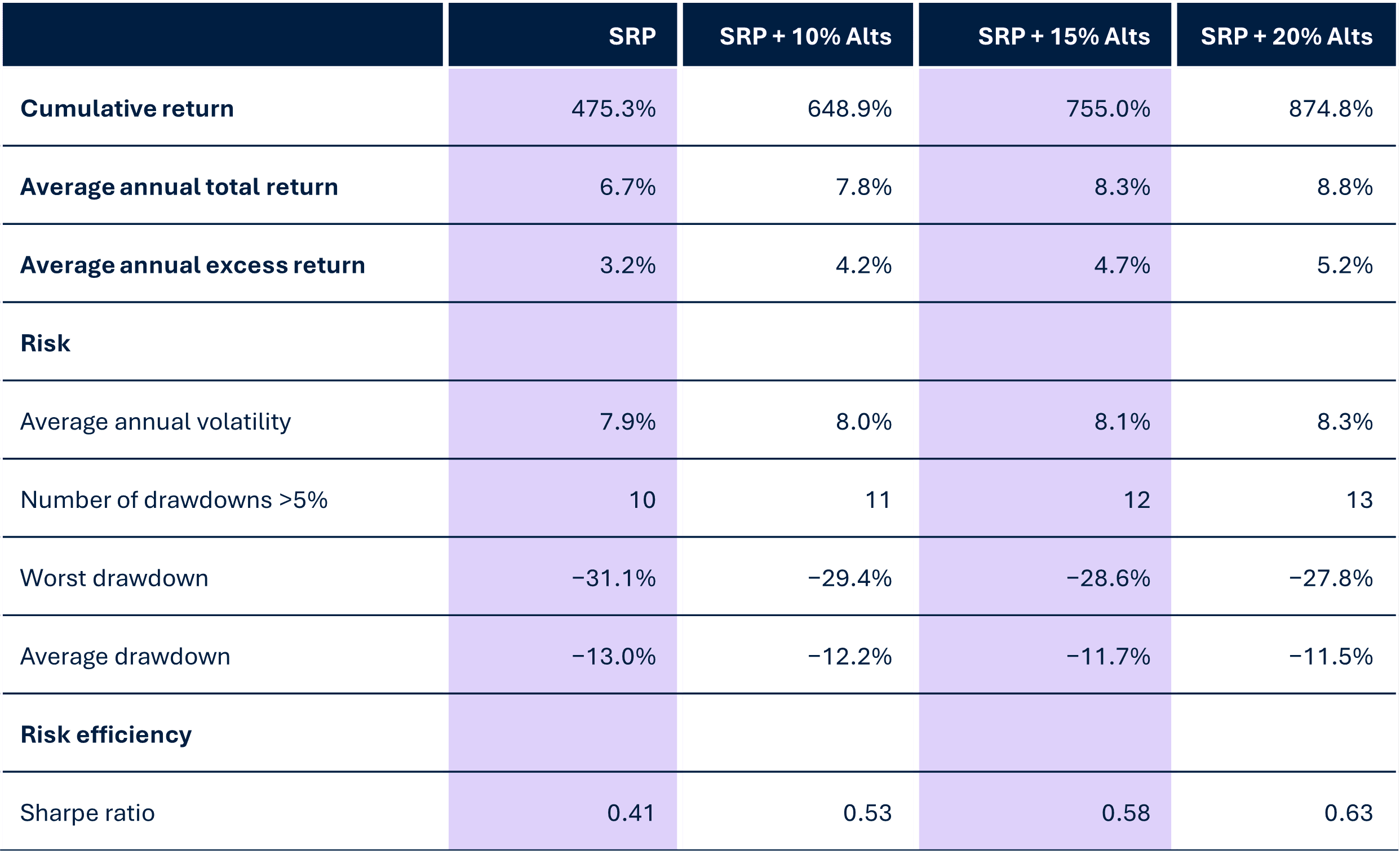

To ground the Alternative Diversifiers™ concept in observed data, we begin with a historical backtest from 1 April 2015 through to December 2025, using monthly rebalancing at month-end. We start here because this is the first period for which we have consistent data for all components of the proposed alternatives sleeve, including Bitcoin. That makes it the cleanest and most meaningful “like-for-like” comparison of the full portfolio design.

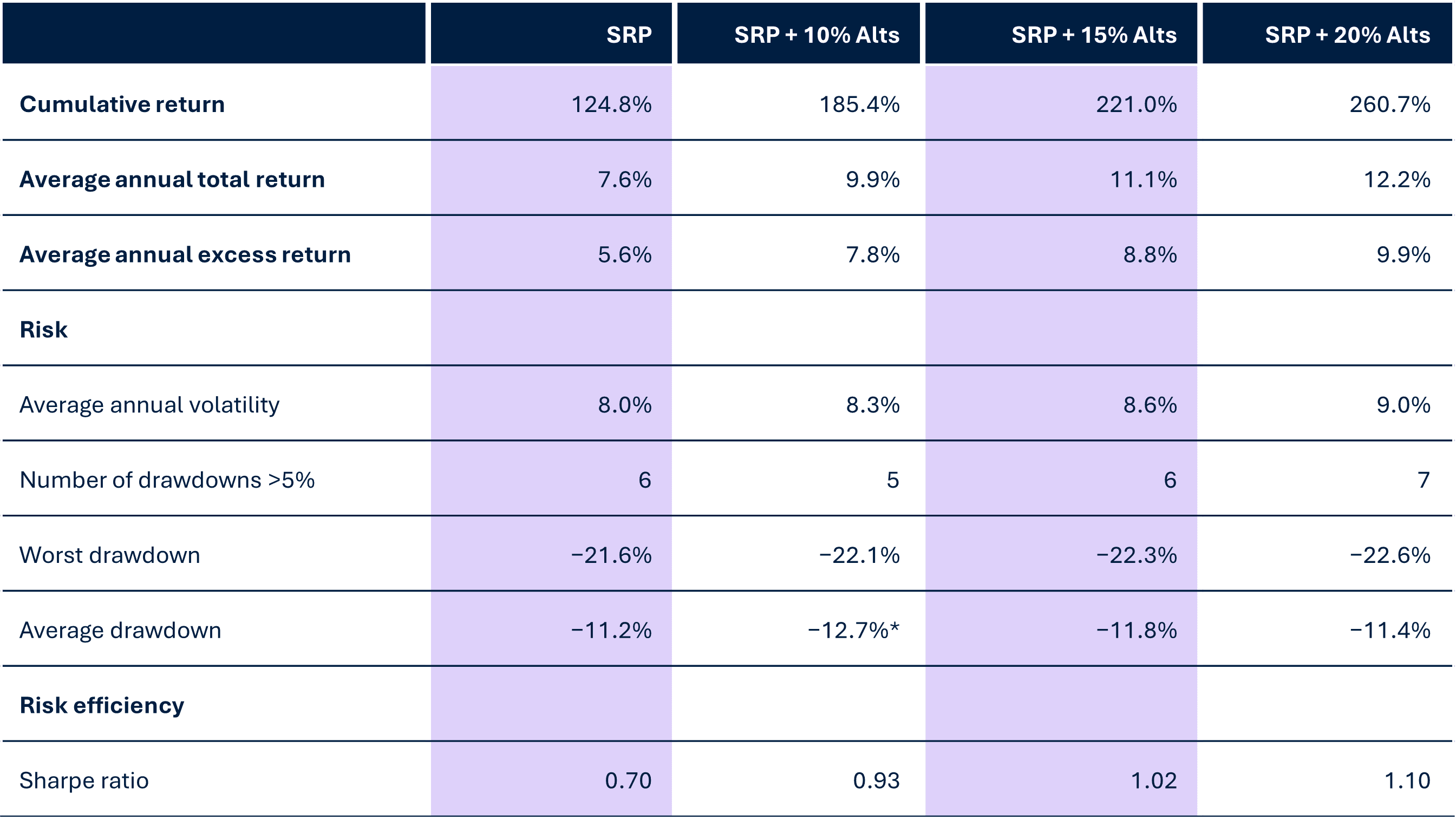

We compare the Simple Reference Portfolio (SRP) from Part 3 against versions that allocate 10%, 15% and 20% to an alternatives sleeve comprising SouthPeak Protection, gold, SG Trend and Bitcoin (equal weighted), funded pro-rata from the SRP’s defensive allocation (Australian bonds, global bonds and cash). This equally weighted allocation serves as a simple baseline against which we will compare more practical weighting approaches later.

* The average is higher because there was one fewer drawdown of >5%

Source: Bloomberg, SouthPeak. All performance results for Alternative Diversifiers™ (and its components) are hypothetical back test performance results, not actual performance; provided for illustration only (and may not be directly investable). A backtest cannot reflect all of the complexities of actual investing and there are many factors which may have materially affected actual results. See Important information below.

The results are encouraging. Over this period, adding the alternatives sleeve improved portfolio outcomes meaningfully. Returns increased materially as the alternatives allocation rose, while the increase in overall portfolio volatility was comparatively modest. Importantly, the improvement in outcomes was not accompanied by a dramatic deterioration in drawdown experience. In other words, the portfolios with alternatives did not simply lever up risk to generate higher returns, they introduced exposures that behaved differently enough from traditional equity-and-bond risk to improve the overall profile. This is also reflected in the steady improvement in risk-adjusted returns across the alternatives allocations.

The cumulative performance chart helps illustrate the effect visually. The alternatives portfolios generally track the SRP over time, but they tend to pull ahead during periods where diversification and non-traditional return drivers matter most. By the end of the sample, higher allocations to the alternatives sleeve correspond to a meaningfully higher terminal portfolio value.

Performance of SRP vs. SRP + alts (equal weight) at 10%, 15% and 20% alts allocation (2015-25)

Source: Bloomberg, SouthPeak. Performance indexed to $100 as at 1 April 2015.

A caveat is that this window, while useful and internally consistent, is still relatively short. It includes important regimes like the COVID shock, the inflation/rates reset, and Bitcoin’s maturation into a more institutionally accessible asset but it remains only a little over a decade of history. For that reason, the next section extends the analysis back to the start of 2000, using the same framework, so we can test the broader logic of the portfolio design over a longer and more varied market history.

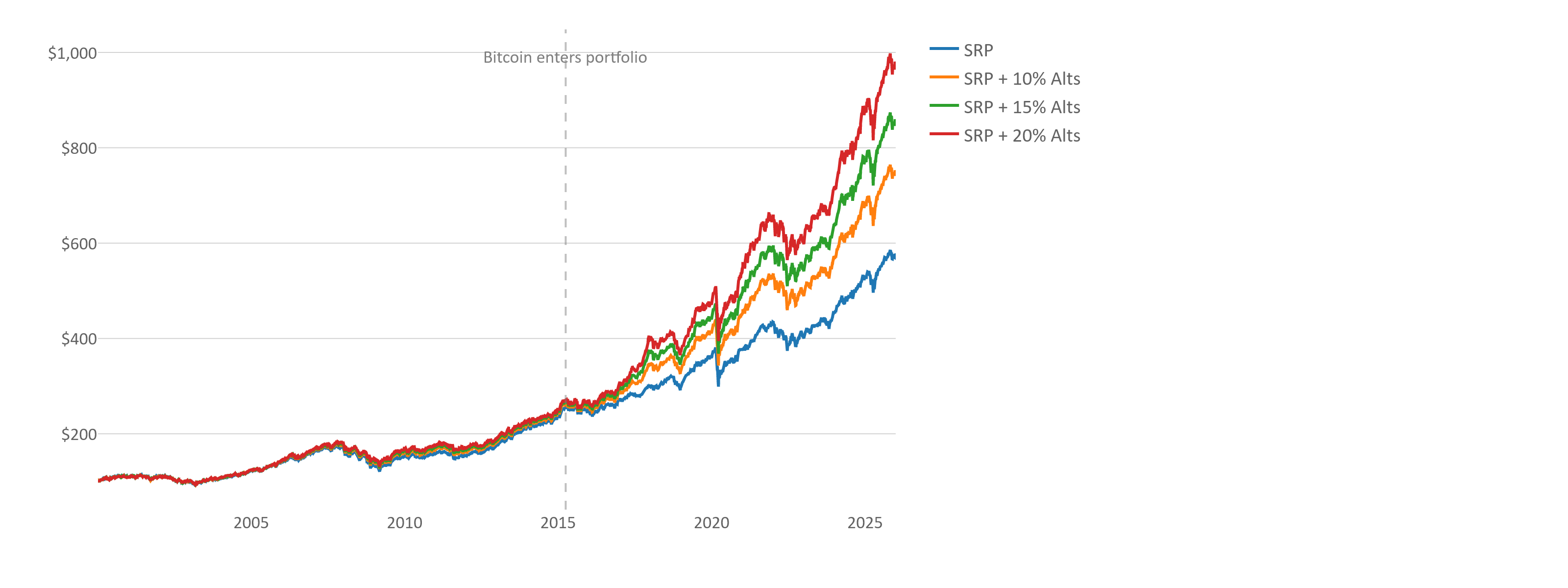

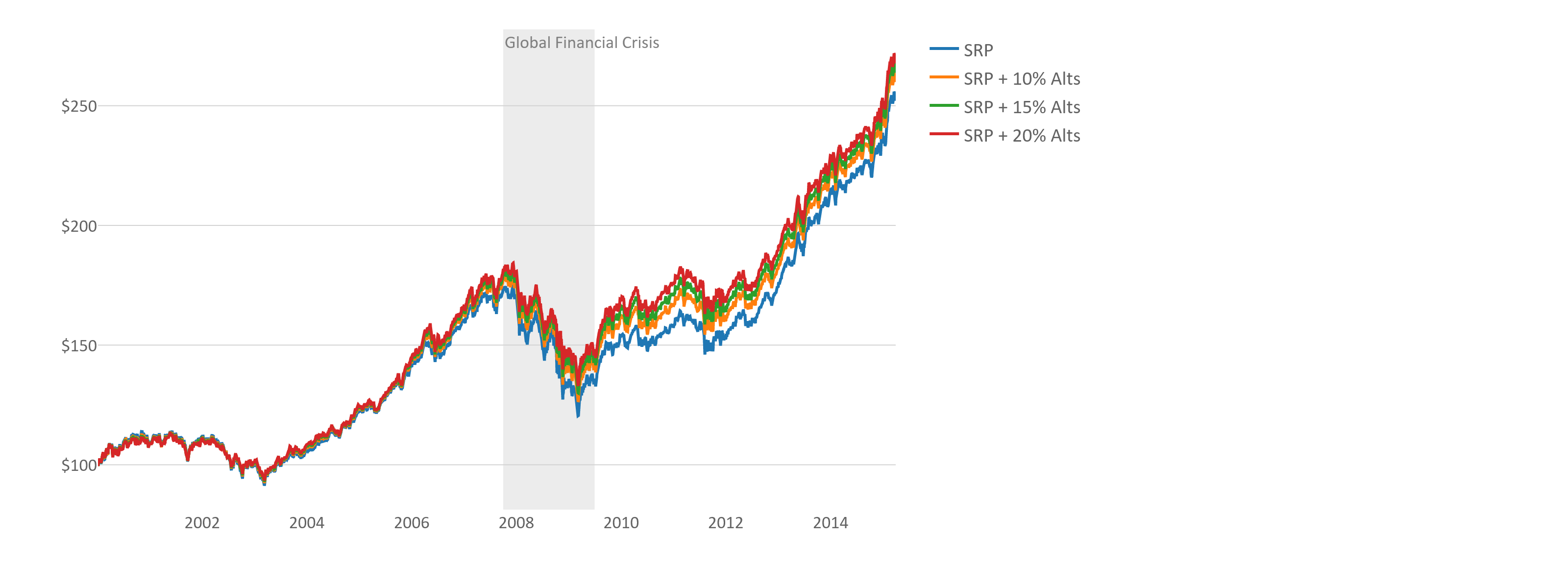

Historical Performance (2000-2025)

Because Bitcoin is not included until April 2015, the alternatives sleeve is handled in two stages: before April 2015, the alternatives allocation is split equally across Gold, SG Trend and SouthPeak (one-third each); from April 2015 onward, it is split equally across all four alternatives, including Bitcoin (one-quarter each). This preserves a consistent total alternatives allocation through time while avoiding the use of pre-2015 Bitcoin data.

Source: Bloomberg, SouthPeak.

Performance of SRP vs. SRP + alts (equal weight) at 10%, 15% and 20% alts allocation (2000-25)

Source: Bloomberg, SouthPeak. Performance indexed to $100 as at 5 January 2000

The long-run results remain supportive of the core thesis. Portfolios with an alternatives sleeve delivered higher cumulative returns and better risk efficiency than the SRP alone over the full 2000–2025 period. However, it is important to be precise about what is driving that result. Most of the performance gap opens up after April 2015, when Bitcoin is introduced into the sleeve. That is visible in the growth chart and is unsurprising given Bitcoin’s exceptional realised returns over that period.

That observation does not undermine the broader portfolio construction case. It simply means we need to separate and test two distinct claims:

- Bitcoin has been the largest contributor to return uplift since 2015; and

- The non-Bitcoin alternatives (Gold, SG Trend and SouthPeak) still provide diversification and protection benefits in important regimes, even without Bitcoin.

To make that distinction clear, we also included in appendix A an analysis that excludes Bitcoin entirely:

- a 2000–2015 comparison (before Bitcoin enters), and

- a 2000–2025 comparison excluding Bitcoin (Gold, SG Trend and SouthPeak only).

These appendix results show a more modest uplift than the main 2000–2025 analysis, but they are still informative. In particular, the alternatives sleeve performs perceptibly better through and after the Global Financial Crisis and again improves relative outcomes in the post-2021 period when bonds became a less reliable diversifier for equities in the portfolio. In other words, the non-Bitcoin sleeve does not dominate long-run returns, but it does improve portfolio behaviour in the regimes where traditional defensive assets can struggle.

This is exactly the rationale for the “diversification of diversifiers” framework. The alternatives sleeve is not designed as a single factor bet. It combines assets that have historically helped in crisis or stress episodes (e.g., Gold, SG Trend, protection strategies), and an emerging store-of-value asset with asymmetric upside potential (Bitcoin).

That naturally leads to the next step in the analysis. Rather than only comparing long-run compounded returns, we examine how each component behaved during specific crisis periods and stress regimes, including episodes where equities fell sharply and periods where bonds did not provide their usual protection.

Crises Performance

The goal of the alternatives sleeve is to improve portfolio resilience and to improve resilience you need assets that perform differently across different types of market shocks. That is exactly what we observe when looking at the performance of the components of the alternatives sleeve during different crises from 2000-2025. Rather than treating all “defensive” assets as interchangeable, the results show that each component tends to protect for a different reason:

- Gold behaves most consistently as a traditional safe haven, particularly in sovereign/currency stress and prolonged uncertainty.

- SG Trend behaves like “crisis alpha,” often performing best when markets experience sustained, directional moves.

- SouthPeak Protection provides the most explicit downside protection, with its strongest results typically occurring in sharp drawdowns and volatility spikes.

- Bitcoin behaves differently from the other three: it has generally not been a reliable short-term crisis hedge, but rather a long-term store-of-value exposure with asymmetric upside and sensitivity to post-crisis liquidity and monetary conditions.

This is the core idea behind the sleeve: diversification within the diversifiers. No single alternative works in every crisis, but a combination can create a more robust portfolio than relying on any one hedge.

Crisis-by-crisis evidence

Across the major crises in our analysis equities are usually the source of drawdown while protection comes from different assets at different times.

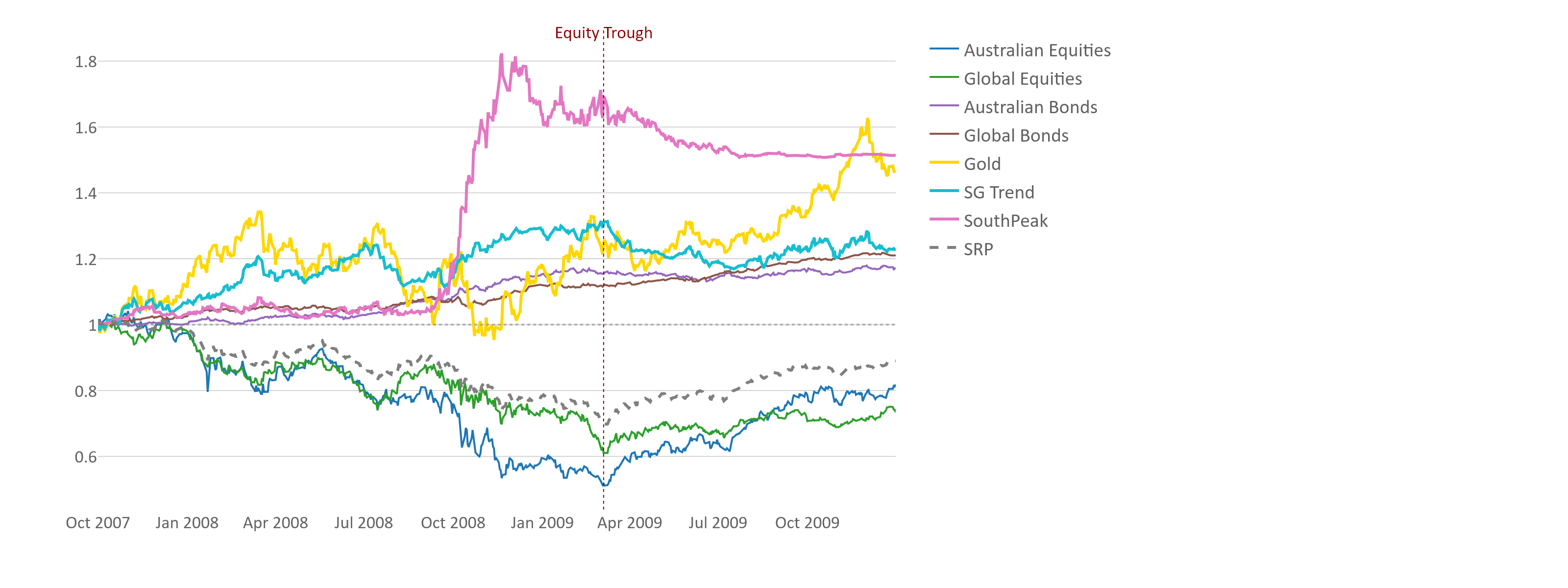

Global Financial Crisis

Source: Bloomberg, SouthPeak. Performance indexed to 1 as at 1 October 2007

During the Global Financial Crisis equities fell sharply, the SRP suffered a large drawdown, and the strongest protection came from SouthPeak, SG Trend, and gold. Bonds also helped, as one would expect in a classic disinflationary shock. This is an important reference case because it illustrates a regime where traditional bond hedging still worked well but the alternatives sleeve added a distinct and valuable source of protection.

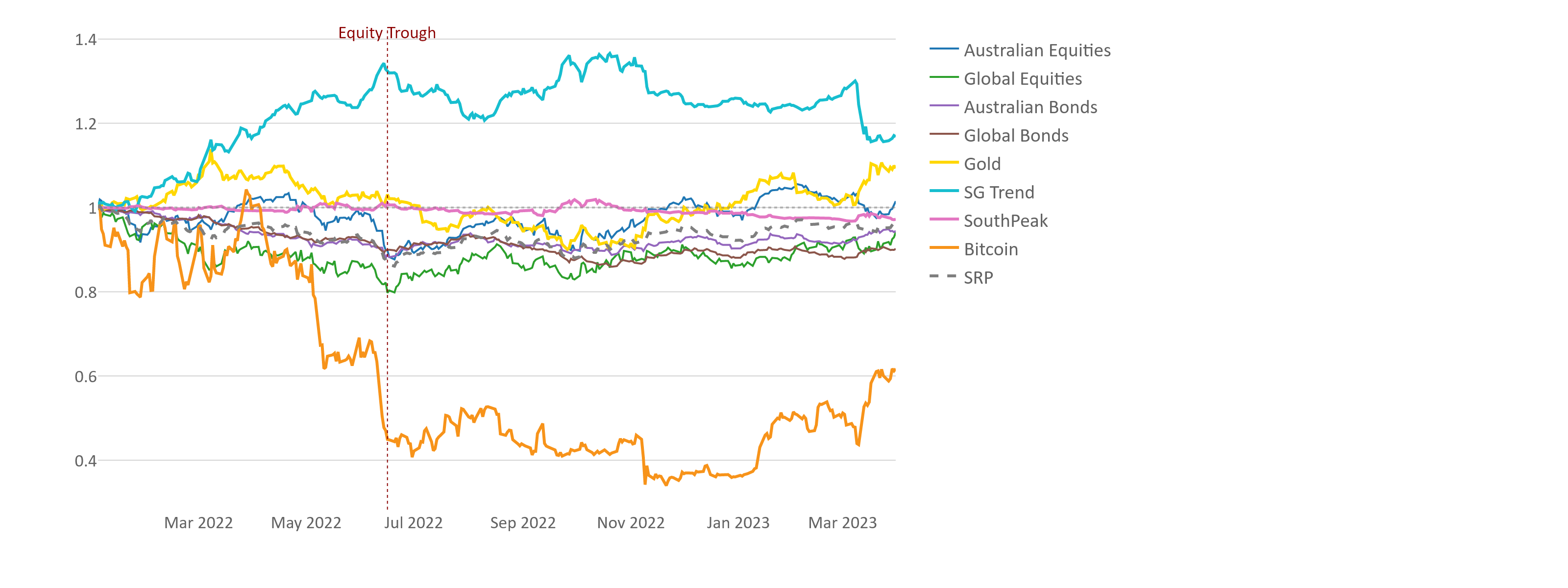

2022 Rate Hike Selloff

Source: Bloomberg, SouthPeak. Performance indexed to 1 as at 3 January 2022

By contrast, the 2022 rate-hike selloff shows why relying solely on bonds as the defensive sleeve is increasingly fragile. In that episode, both equities and bonds fell together. Gold was mixed, Bitcoin fell sharply, but SG Trend and (to a lesser extent) SouthPeak provided the most meaningful offset. This is exactly the type of environment that motivates a broader alternatives sleeve: when the traditional stock/bond diversification relationship weakens, investors need other forms of convexity and crisis diversification.

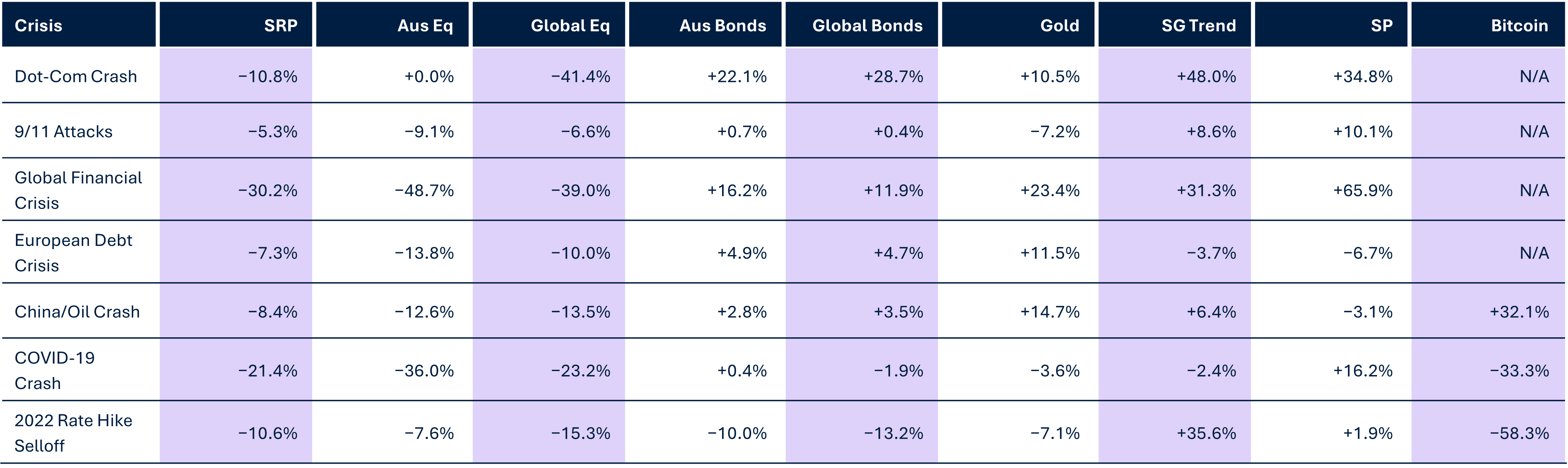

Across all crises from 2000-2025 the performance of each asset was the following:

Source: Bloomberg, SouthPeak

The crisis return table reinforces the visual evidence:

- SouthPeak and SG Trend were the strongest average performers across crisis periods.

- Gold was positive in four out of seven crises and offered a steadier, traditional hedge profile.

- Bitcoin was highly regime-dependent: strong in some post-2015 episodes (e.g., China/Oil), but weak in liquidity-driven stress (e.g., COVID, 2022).

- The SRP itself delivered negative returns in every crisis period in the table, which is precisely why a complementary sleeve is needed.

The takeaway is that a protection sleeve shouldn’t rely on any one alternative as “the answer” but on a variety of protection mechanisms that react differently and therefore complementary in a crisis.

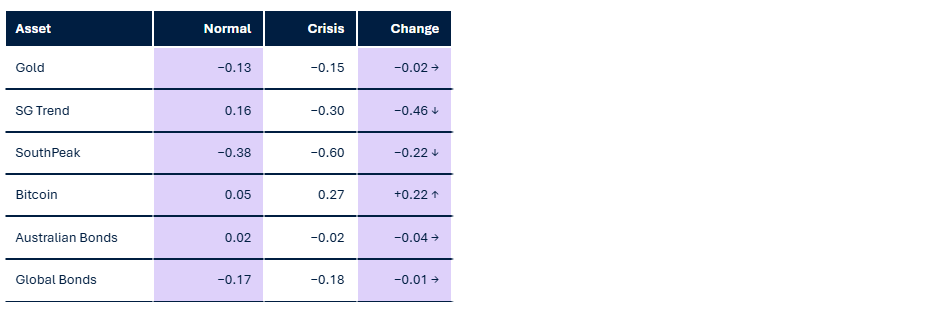

The following table shows the correlations of each asset with global equities during normal times as well as crises:

↑ = Correlation increases (less protective during crisis), ↓ = Correlation decreases (more protective during crisis), → = Correlation stable

The correlation analysis highlights that during crises, some alternatives become more protective (their correlation to global equities falls), while others become less protective. For example, SouthPeak’s correlation to global equities becomes more negative during stress, which is what we would expect from explicit tail-risk hedging. Bitcoin, on the other hand, tends to become more positively correlated to equities in acute selloffs, reinforcing the point that its role is not short-term crisis protection.

This distinction matters for portfolio construction. A robust alternatives sleeve should not be designed around a single narrative (“safe haven” or “digital gold”), but around multiple, distinct protection channels.

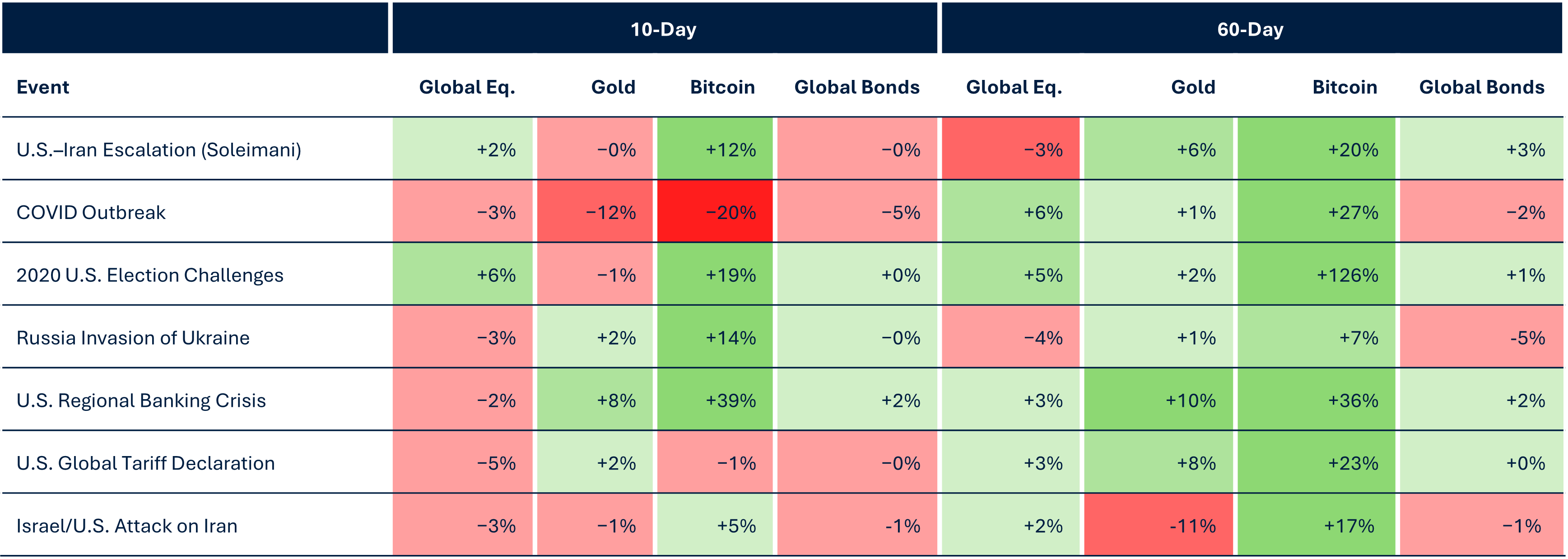

In their paper “Bitcoin: A Unique Diversifier”, originally published in September 2024, Blackrock analysed the performance of Bitcoin, gold and the S&P 500 10 days and 60 days after some of the most disruptive global events since 2020. Blackrock found that, despite an initial strong sell-off, Bitcoin recovered better and faster than gold or the S&P 500 in most cases. Borrowing this framework, we replicated the analysis using global equities instead of the S&P 500 and included global bonds. We also added the most recent disruptive global event, the Israel/US attack on Iran to the analysis. The performance across the assets and events is the following:

Source: Bloomberg

10 days after each of these disruptive events, Bitcoin was the best performing asset 5 out of 7 times and 60 days after each event Bitcoin was the best performing every time.

This raises the question whether Bitcoin is already starting to serve as a digital “flight to safety” asset, or at least as a useful diversifier during times of uncertainty, since 2020. The crisis analysis above focuses on major equity-led stress events. The next question is even more relevant for today’s portfolio construction problem: what happens when both equities and bonds struggle at the same time? That is the environment in which traditional diversification is least reliable, and where the case for a broader alternatives sleeve becomes strongest.

When equities and bonds fall together

One of the central assumptions in traditional portfolio construction is that bonds provide offsetting returns when equities fall. Over much of the last four decades that was a reasonable assumption. But it is not a law of nature. In inflationary or policy-driven regimes, equities and bonds can decline together, leaving a conventional diversified portfolio more exposed than many investors expect.

Because this article proposes funding the alternatives sleeve from the defensive side of the portfolio, it is important to test exactly this failure mode, i.e. when traditional bond-equity diversification breaks down, which assets have actually provided protection?

To answer that, we split the analysis into two periods. For pre-2000 episodes (where data availability is more limited), we focus on gold, global equities and global bonds, using a synthetic extension of global bond returns built from historical US 10-year Treasury yields. From 2000 onward, we use the full dataset and include the other alternatives, with Bitcoin included from April 2015.

The pre-2000 evidence is especially useful because it captures a set of market environments that many investors today have not experienced directly, particularly inflation-linked stress episodes.

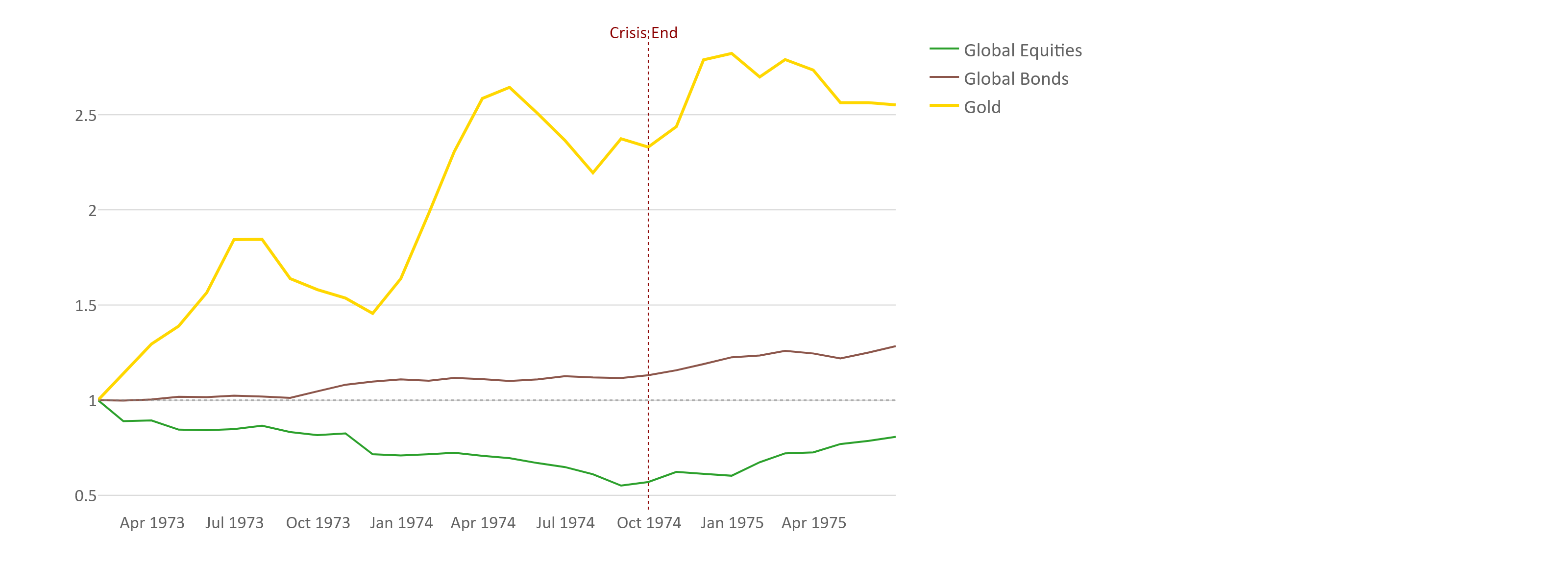

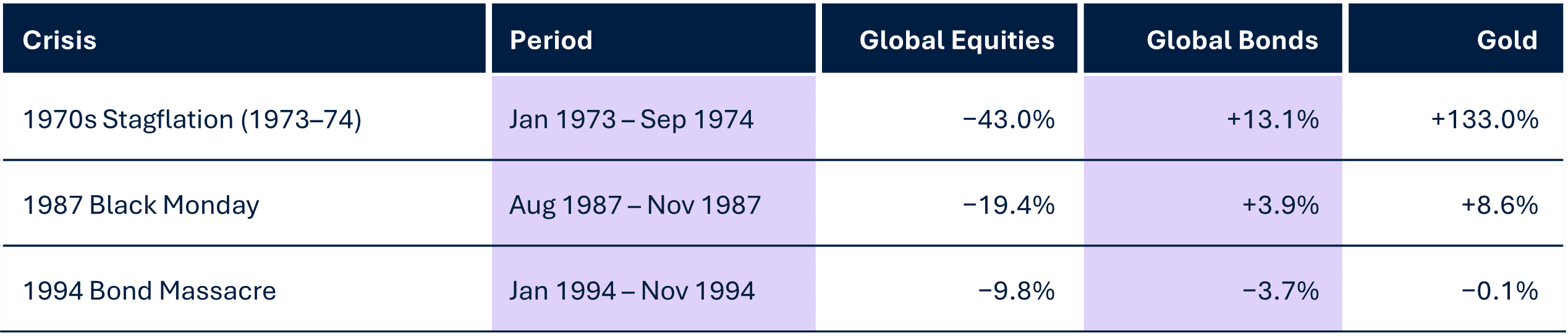

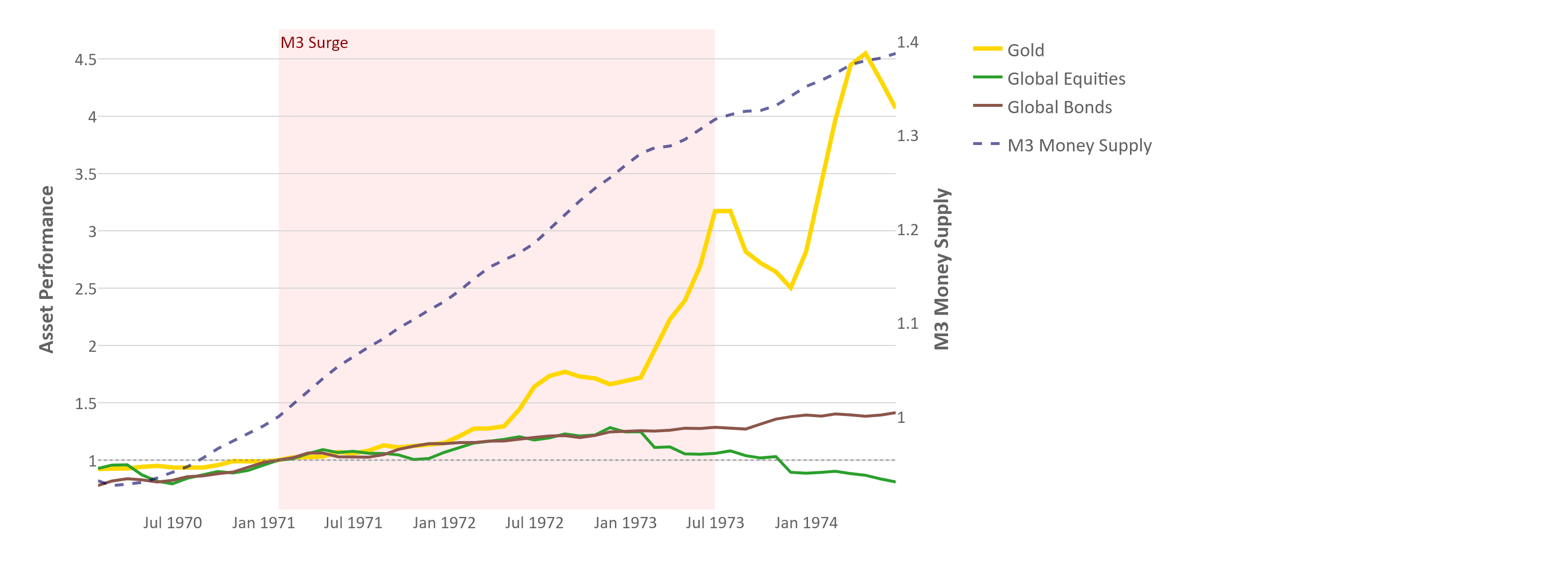

1970s Stagflation (1973-74)

In the 1970s stagflation period (1973–74), both equities and bonds struggled while inflation remained elevated. The chart and summary table show that equities fell heavily, bonds delivered only modest positive returns, and gold strongly outperformed. This is precisely the type of regime in which traditional diversification weakens, and monetary instability becomes central to asset performance.

Source: Bloomberg. Performance indexed to 1 as at 31 January 1973

Source: Bloomberg

1987 and 1994: contrasting crises

The 1987 crash and 1994 bond massacre provide a useful contrast. In 1987, bonds still helped and gold was positive but less decisive. In 1994, bonds themselves came under pressure, and gold was comparatively more resilient than equities. Taken together, these episodes reinforce the point that the best hedge depends on the nature of the shock, but gold repeatedly appears as a relevant diversifier when inflation and policy stress erode the reliability of bonds.

The post-2000 analysis shows that once we move beyond the old disinflationary regime, protection becomes much more conditional.

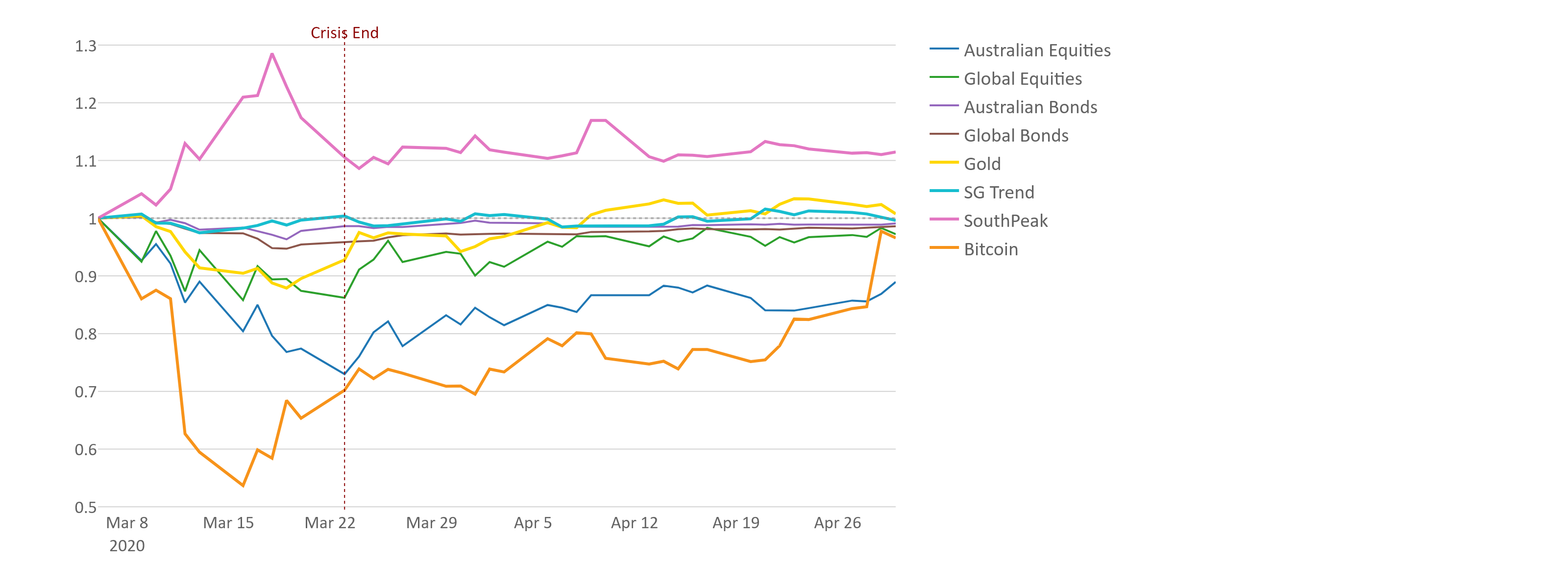

COVID-19 Liquidity Crisis (March 2020)

The COVID liquidity crisis (March 2020) is a good reminder that in acute “dash-for-cash” environments, even assets often thought of as hedges can sell off temporarily. In that episode, both gold and bonds were less effective at the peak of stress than many would expect, while explicit protection strategies such as SouthPeak held up much better. This is exactly the type of scenario where a dedicated tail-risk sleeve can add value relative to relying on traditional safe havens alone.

Source: Bloomberg, SouthPeak. Performance indexed to 1 as at 68 March 2020

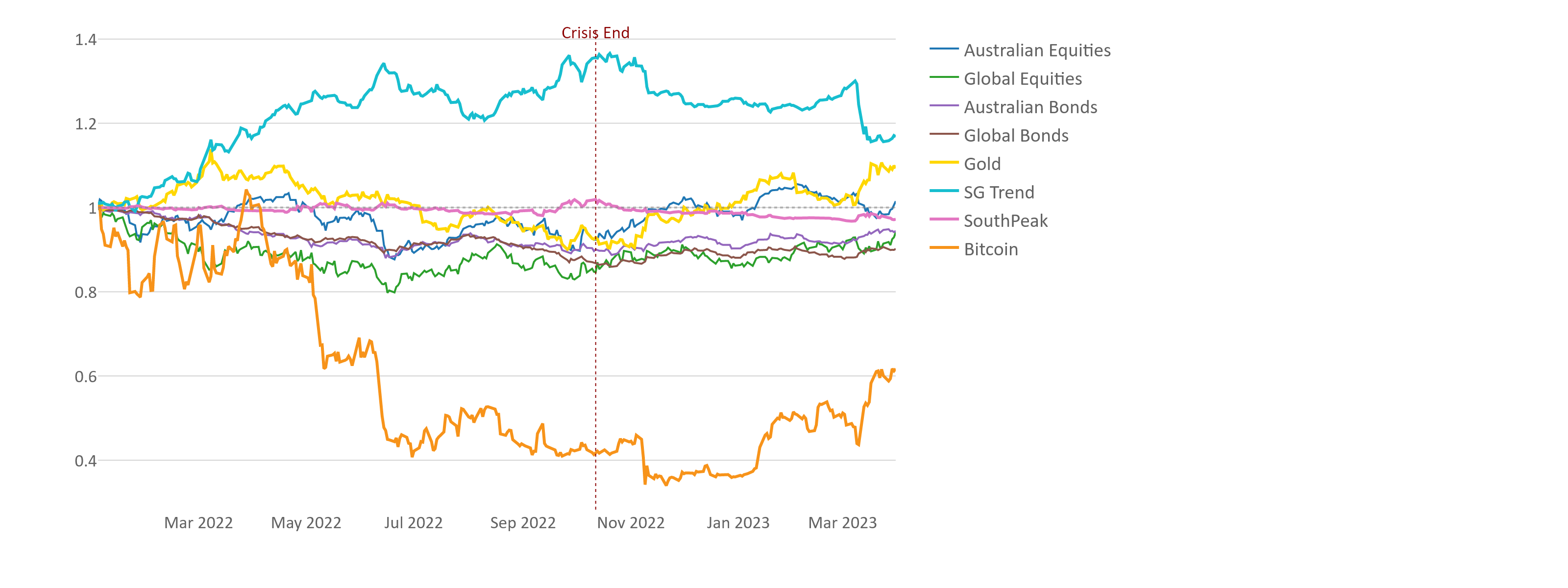

2022 rate hike selloff

The 2022 rate-hike selloff is arguably the most important episode for today’s portfolio construction debate. It is one of the clearest modern examples of a simultaneous equity-bond drawdown driven by inflation and aggressive monetary tightening. In this regime, the chart shows that bonds did not provide the defensive offset investors had become used to. By contrast, SG Trend performed strongly, while gold was mixed but improved later in the period.

Source: Bloomberg, SouthPeak. Performance indexed to 1 as at 3 January 2022

Store of value assets during monetary expansion

The crisis analysis in the prior sections shows why a diversified alternatives sleeve can improve resilience during equity drawdowns and periods when traditional bond-equity diversification fails. But that is only part of the story.

The broader thesis of this series is not simply about crisis protection. It is about stores of value - assets that can help preserve purchasing power when fiat money supply expands materially over time.

Gold and Bitcoin should not be judged primarily on whether they hedge every equity selloff but whether they protect against monetary debasement and the erosion of real value that can follow sustained money creation. Gold is the long-standing analogue, and Bitcoin is the emerging digital version of that proposition, with the added feature of asymmetric upside if adoption as a global store of value continues consistent with current trends

Periods of rapidly increasing money supply and the downstream inflationary consequences are precisely where bonds are likely to fail as a diversifier when measured in inflation-adjusted terms.

To examine this directly, we analysed periods of significant US M3 money supply expansion, using broad US money supply (US M36) growth as a proxy for broad monetary conditions. We then compared the performance of portfolio assets through these episodes, including pre-2000 periods (using Gold, Global Equities and Global Bonds) and post-2000 periods (including the full opportunity set, with Bitcoin from April 2015 onward).

The objective here is to isolate episodes where monetary expansion itself was a dominant macro feature. We identify periods where 12-month M3 growth materially exceeded its long-run average and then chart asset performance from before, during and after the expansion window. This broader framing is important because the effects of rapid money growth do not necessarily appear immediately in either consumer prices or asset prices but tend to work through the system with a lag. Correlation analysis, for example, shows only a weak relationship between money supply growth and same-year CPI outcomes, but a meaningfully stronger relationship one and two years later. For that reason, we do not only look at what happened during the period of significant money supply growth, but also at how the monetary debasement risk was building and then being progressively absorbed by markets, which can take 1-2 years.

The pre-Bitcoin episodes are especially useful because they remind us that there is no single macro template for how monetary debasement transmits into markets.

Vietnam/Nixon Era (1971-73)

In the Vietnam/Nixon era (1971–73), which culminated in the closure of the gold window and a major shift in the global monetary system, gold dramatically outperformed while equities and bonds were far weaker. This is exactly the type of environment in which a store-of-value asset should demonstrate its value: a monetary regime shock combined with rising uncertainty around fiat credibility. Importantly, gold’s outperformance did not occur immediately at the start of the money-supply surge. It intensified as the implications of the regime change became clearer and as markets progressively absorbed what the end of gold convertibility meant for fiat money. The strong outperformance of gold materialised over 3 years in this case.

Source: Bloomberg. Performance indexed to “1” as at 31 Jan 1971.

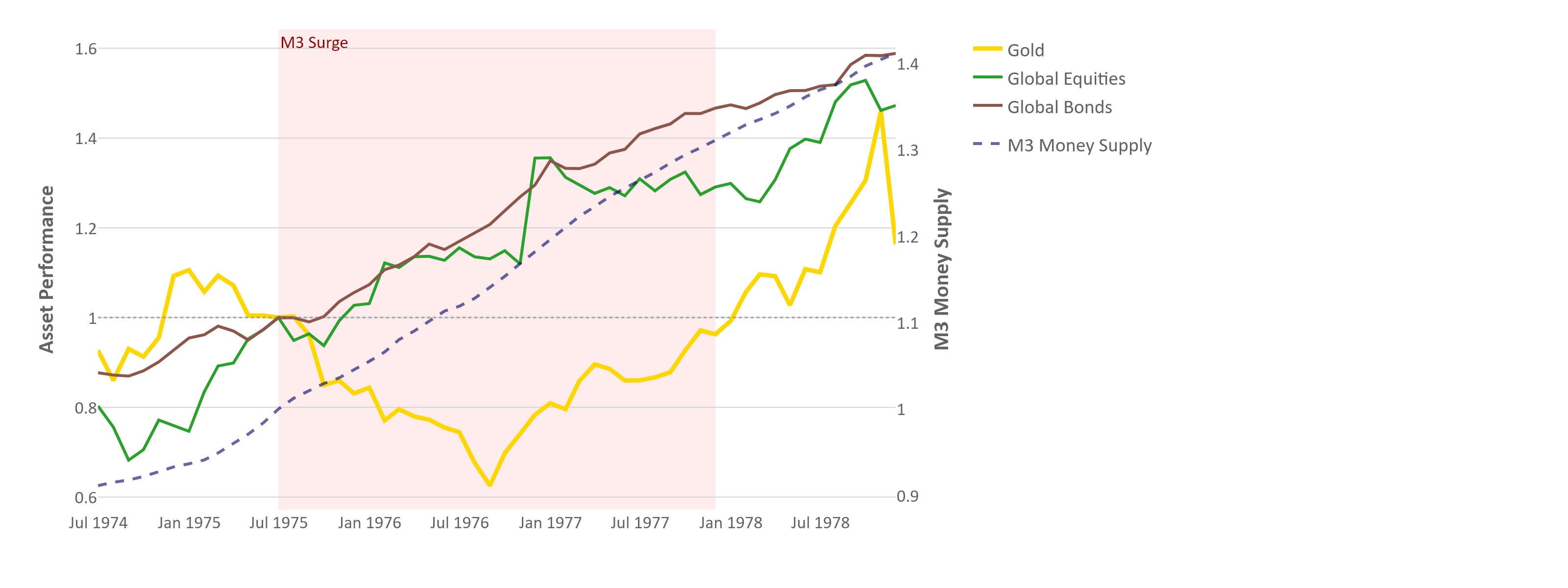

By contrast, in the post-stagflation expansion (1975–78), the signal is more mixed. Gold did not deliver the same immediate payoff, while equities and bonds performed well as policy eased and growth recovered. Here, gold weakened initially, bottomed well into the expansion, and only later recovered strongly. This is an important reminder that the transmission from money supply growth to inflation expectations, real yields, policy credibility and risk appetite varies by regime. In some episodes, monetary expansion first supports financial assets more broadly before its consequences are reflected in inflation-sensitive stores of value.

Post-Stagflation Expansion (1975-78)

Source: Bloomberg. Performance indexed to “1” as at 30 June 1975.

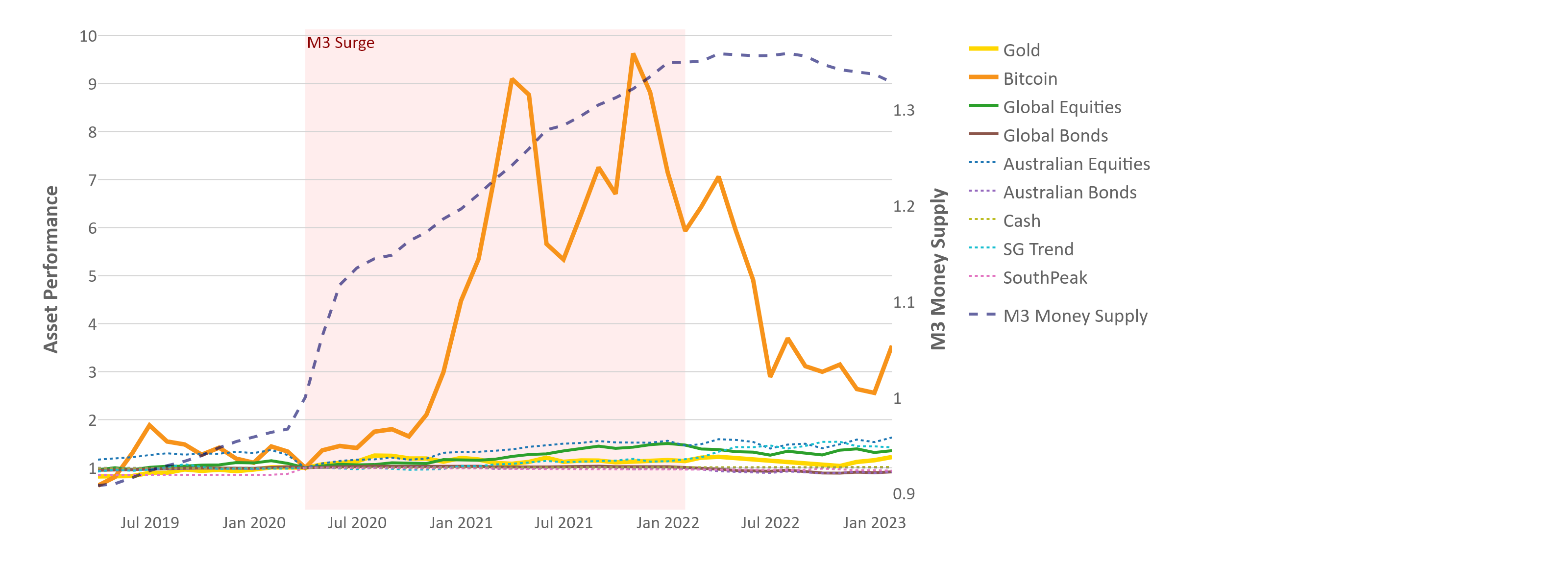

The COVID stimulus period (2020–22) is the clearest modern example of the framework in this article series. It combined extraordinary fiscal expansion with the fastest broad money growth in the sample. In that environment, the performance dispersion across assets is highly informative.

Bitcoin’s response during this period was much faster and more explosive than gold’s response in the 1970s monetary-expansion episodes. In our view, this reflects a combination of market structure, asset maturity and the nature of the policy shock itself. First, modern financial markets process macro information far more quickly than they did in the 1970s. During COVID, investors could observe the scale of fiscal transfers, quantitative easing and money-supply growth in near real time and reprice assets almost immediately. Second, in 2020–21 Bitcoin was still a relatively small (~$100B market cap) and highly reflexive market, meaning that changes in narrative and capital flows had a much larger effect on price than they would in a far larger and more established asset such as gold. Third, the COVID-era expansion was unusually direct and visible, combining monetary easing with explicit fiscal stimulus and transfer payments, whereas the 1970s episodes involved a slower and messier interaction between policy, dawning understanding of the impacts of what was a relatively new policy, inflation and ultimately confidence in the monetary regime. In 2020-21, gold behaved more like a mature incumbent store of value, responding gradually as the inflationary and monetary consequences became clearer over time whereas Bitcoin behaved like a higher-beta, emerging digital store of value, with a much faster and more amplified response to the same broad debasement thesis.

COVID Stimulus (2020-22)

Source: Bloomberg, SouthPeak. Performance indexed to “1” as at 31 March 2020.

It is also worth noting that Bitcoin suffered a sharp drawdown after the peak of the COVID-era monetary expansion. In our view, that decline does not invalidate the debasement thesis but reflects the fact that Bitcoin is still an emerging and highly volatile asset that can be strongly affected by tighter liquidity and industry-specific shocks. The 2022 bear market was shaped by a combination of aggressive global monetary tightening, the collapse of Terra/Luna and related crypto-credit failures, and later the failure of FTX, which severely damaged confidence across the sector. In other words, Bitcoin responded strongly to the surge in monetary expansion, but its subsequent drawdown reflected both macro tightening and crypto-specific deleveraging rather than a simple reversal of the long-run store-of-value narrative.

Taken together, these monetary-expansion episodes strengthen the case for treating Gold and Bitcoin as a distinct part of the alternatives sleeve. The crisis analyses in earlier sections showed that Bitcoin is not a reliable short-term equity hedge and the monetary-expansion analysis helps explain why that is the wrong benchmark. Bitcoin’s role is not to protect portfolios in every panic but to provide exposure to a digital, scarce, non-sovereign store-of-value asset that can benefit materially if fiat debasement concerns intensify over time.

Gold, meanwhile, remains the proven incumbent non-sovereign store-of-value asset. It has shown over multiple decades that it can perform strongly in periods of monetary disorder and declining confidence in fiat anchors, even if the timing and magnitude of its response varies across cycles.

This is also why we continue to believe the combination matters more than either asset in isolation. Gold and Bitcoin express the same broad store-of-value theme, but with very different maturity, volatility and return profiles. In portfolio terms, combination creates a more robust exposure than a single-asset bet.

Alternative Diversifiers™ in Practice

The historical analyses above use an equal-weight allocation across the four alternatives components because it is simple and transparent. But it is not the only plausible implementation, and it is not necessarily how many professional investors would size the sleeve in practice. One of the key reasons why investors might weight the four components differently is because they do not play the same role and do not carry the same volatility. In particular, gold and Bitcoin both express the broad store-of-value theme, but in very different ways, as we have outlined in previous articles. The allocation between gold and Bitcoin within this store-of-value component of the sleeve would likely reflect these differences.

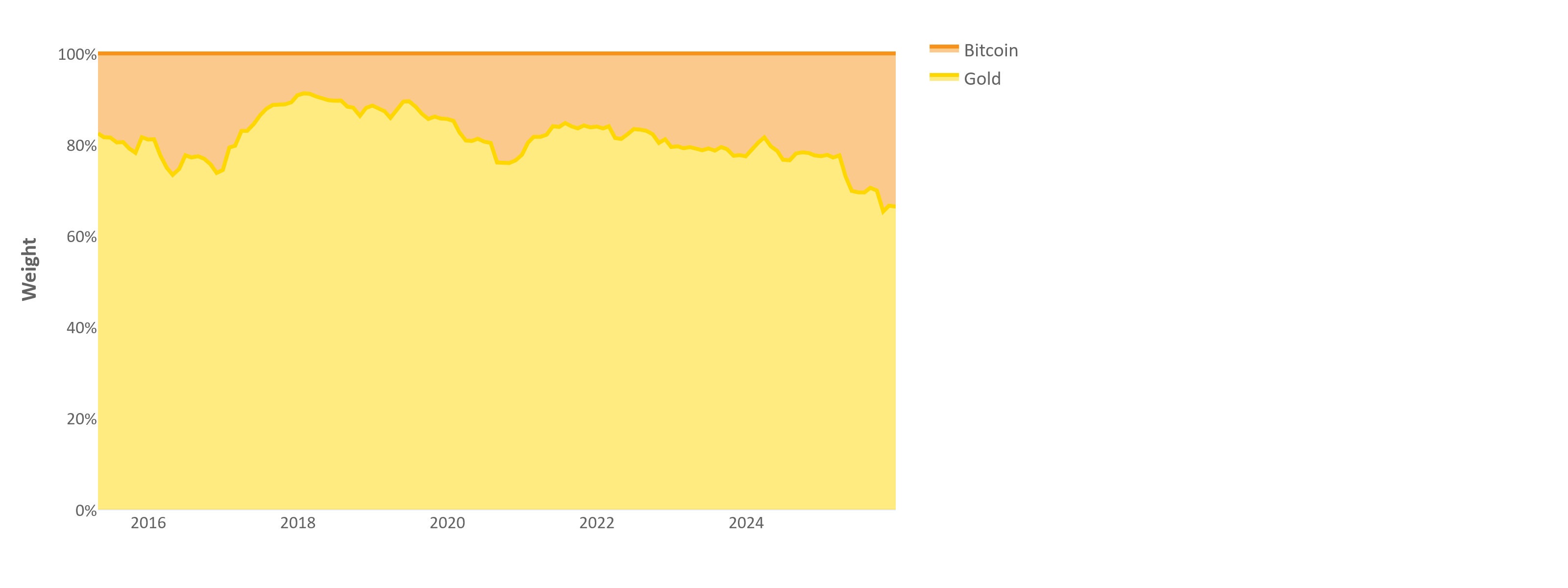

One way that investors could reflect this in their allocation is to group gold and Bitcoin into a single store-of-value (SoV) sleeve, with the two allocation to each of the assets weighted inversely by their respective volatility. This results in a more realistic exposure to the SoV theme, with gold receiving around 80% of the SoV weight and Bitcoin receiving 20%, when weighted inversely based on a rolling volatility measure.

Store-of-value inverse-volatility weights over time (2015-25)

Source: Bloomberg

Once Gold and Bitcoin are grouped into SoV, the alternatives sleeve can be viewed as having three functional components:

- SouthPeak Protection: explicit downside protection / tail-risk hedging

- SG Trend: crisis alpha through trend capture

- SoV: long-term monetary debasement hedge through gold and Bitcoin

From this perspective, there is no single “correct” way to size the sleeve. Different investors may prefer different balances depending on their tolerance for carry drag, their conviction on SoV assets, and the role they want the sleeve to play inside the broader portfolio. To illustrate this, we consider two practical examples.

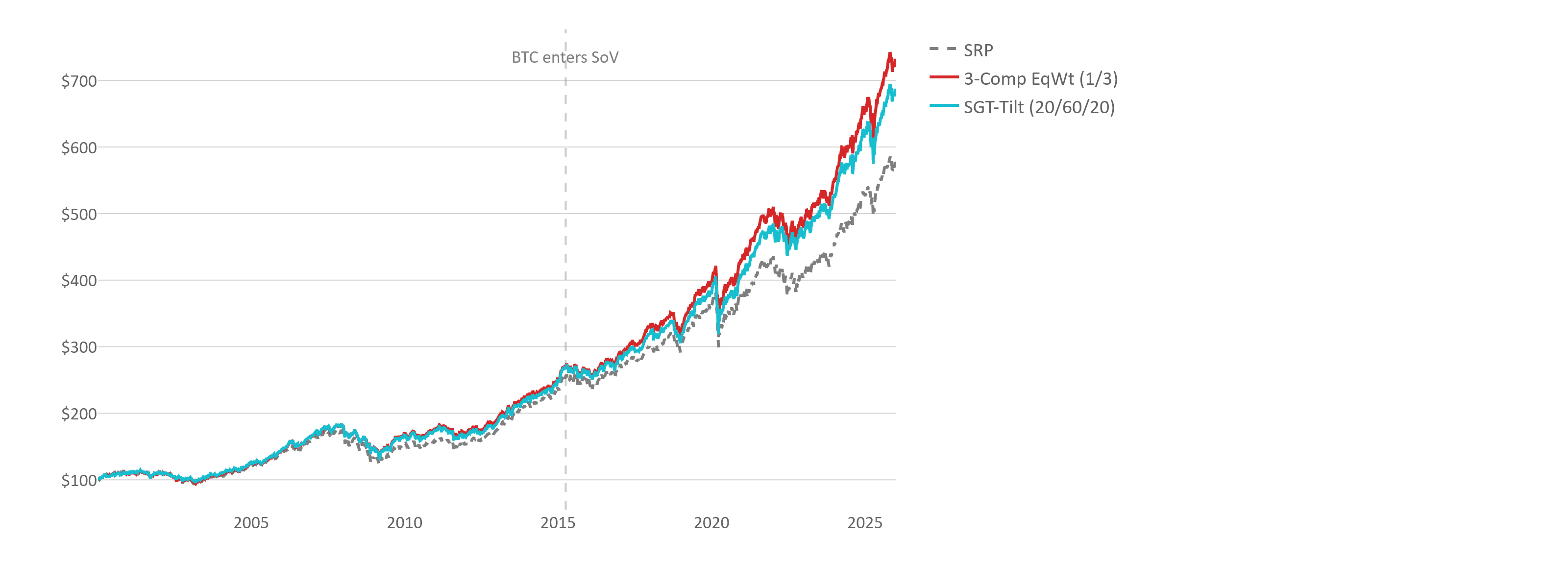

The first is a three-sleeve equal-weight implementation, which allocates one-third each to SouthPeak, SG Trend and SoV. This retains the simplicity of equal weighting but does so at the level of functional sleeves rather than at the level of individual assets.

The second is a more practitioner-style implementation, with 60% SG Trend, 20% SouthPeak and 20% SoV. The intuition here is that trend-following often warrants a larger structural allocation than explicit tail hedging because it can participate more broadly across sustained crisis and inflation regimes with less persistent carry drag than long-volatility strategies. SouthPeak remains meaningful because explicit convex downside protection is still valuable but is sized more conservatively to reflect the ongoing cost of insurance. SoV remains a distinct sleeve because store-of-value exposure addresses a different portfolio risk from crisis alpha or tail hedging.

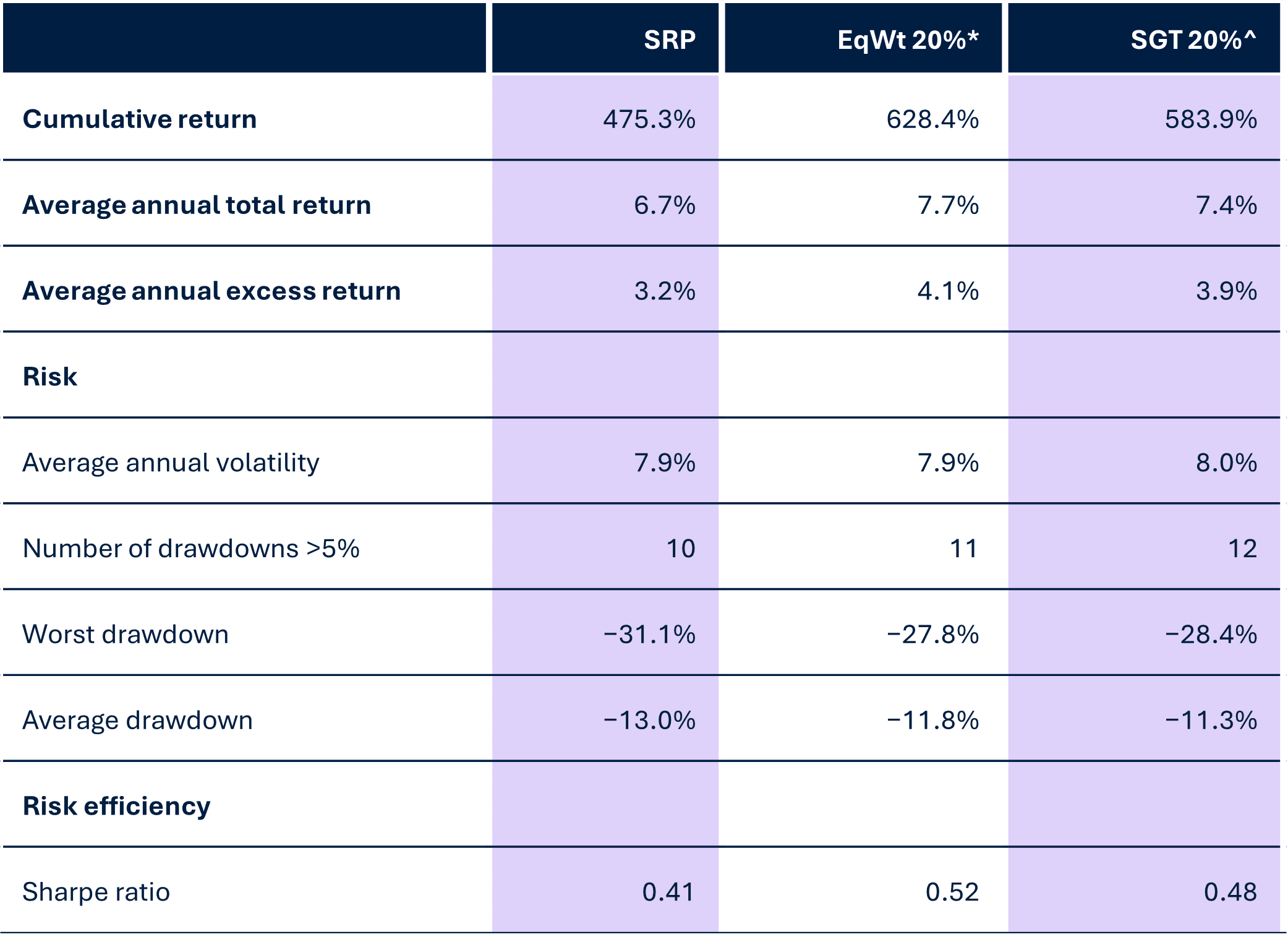

Compared to the standalone SRP and the baseline model with equal weight across all four alternatives assets the performance of these two approaches is the following at a 20% alternatives allocation:

Performance of SRP vs. practitioner-style alts implementations at 20% alts allocation (2000-25)

Source: Bloomberg, SouthPeak. Performance indexed to $100 at 5 Jan 2000.

Source: Bloomberg, SouthPeak

*EqWt 20% = 20% allocation to: 1⁄3 SG Trend, 1⁄3 SouthPeak and 1⁄3 SoV

^SGT 20% = 20% allocation to: 60% SG Trend, 20% SouthPeak and 20% SoV

Both practical versions improve on the SRP standalone performance. Between the two, the equally weighted approach performed better than the SG-tilted approach due to the alternatives component with the strongest historical performance, the SoV sleeve, receiving a larger allocation.

These two practical implementations are examples of how investors might think about allocating between diversifiers that serve different purposes alongside assets that traditionally make up diversified portfolios. The precise balance will ultimately depend on investor objectives, implementation preferences and conviction.

Risks, caveats and governance

Alternative Diversifiers™ are not a free lunch. The main risks are:

- Cost and carry: Long volatility can be expensive in calm markets; implementation should be sized and designed to be sustainable.

- Manager risk: Systematic alpha and protection mandates can vary widely by manager: initial and ongoing due diligence and diversification matter.

- Correlation drift: In liquidity-driven regimes, correlations can converge; monitoring and stress testing should be ongoing.

- Bitcoin-specific risks: Regulatory risk, custody risk, technology risk, and behavioural drawdowns require conservative sizing, clear governance and appropriate disclosure.

- Rebalancing discipline: Without rebalancing, the sleeve can drift into unintended exposures.

A practical governance approach is to define a clear purpose for each sleeve (what it is meant to protect against), set maximum weights and rebalancing rules, and monitor a small set of ‘health indicators’ (such as carry cost for the protection sleeve, realised correlation to equities, and drawdown contributions).

Conclusion

Across this series, we have moved from first principles to practical portfolio construction.

In Part 1, we examined what makes an asset a store of value and why gold has fulfilled that role for centuries. In Part 2, we argued that Bitcoin can be understood as an emerging digital store of value: a scarce, non-sovereign monetary asset whose long-term case is tied not to short-term crisis protection, but to monetary debasement, growing digitisation and continued adoption. In Part 3, we showed that small allocations to store-of-value assets can improve the risk and return profile of a diversified portfolio. And in this final part, we have taken the next step by asking what a broader defensive architecture might look like in a world where bonds may no longer be sufficient on their own.

That is the central message of this article. Investors are facing an environment where inflation may remain structurally higher than it was in the disinflationary era, sovereign debt levels are elevated, and fiat currencies are expected to continue losing purchasing power over time. In that environment, the traditional answer to these risks – a defensive allocation dominated by bonds and cash – may be less reliable than it once was. If that is true, then portfolio construction needs to adapt.

Our answer is a diversified sleeve of diversifiers. In this article, we outlined how the portfolio allocation that traditionally served the role of diversification and portfolio protection can be broadened in a thoughtful and forward-looking way. We also demonstrated that no single component is sufficient on its own, which is precisely why a diversified sleeve matters. The approaches we have outlined here serve as examples of how investors could approach this problem in practice, but we recognise that there is no universally “optimal” implementation. Different investors will reasonably choose different balances depending on their objectives, governance constraints, tolerance for carry drag, and conviction in the store-of-value theme. They may have a preference for different implementations of long volatility and trend following which serve similar purposes to the ones that we identified.

In our view, the store-of-value component of an alternative diversifier sleeve is critical as it provides returns uncorrelated with global equities and directly addresses some of the fundamental reasons behind why bonds may not serve as a reliable hedge to equities going forward, at least not to the extent that they did the last four decades. And of the possible candidates for a store-of-value component we view gold and Bitcoin as the assets that will best fulfil this role, for the reasons why outlined in this series of articles. By combining the two within a store-of-value sleeve, investors stand to benefit from gold’s established role as a store of value and the asymmetric upside of Bitcoin playing an increasingly important role within this market. That, we believe, is the case for gold and Bitcoin in future-oriented diversified portfolios.

Appendix

The charts in this appendix isolate the contribution of the non-Bitcoin alternatives - Gold, SouthPeak, and SG Trend - to test whether the diversification case holds independently of Bitcoin's exceptional returns.

The below chart shows the portfolio growth of the SRP and the three alternatives weightings over the full 2000-2025 period, with Bitcoin excluded entirely.

Performance of SRP vs. SRP + alts excluding Bitcoin (equal weight) at 10%, 15% and 20% alts allocation (2000-25)

Source: Bloomberg, SouthPeak. Performance indexed to $100 as at 5 Jan 2000.

The performance gap is considerably narrower than in the main analysis, confirming that Bitcoin accounts for most of the uplift in returns after April 2015. Nevertheless, a meaningful separation is still visible. The alternatives portfolios pull ahead following COVID, as gold and SG trend provide good returns and SouthPeak offsets the drawdown in other assets during the initial shock. But even prior to April 2015, the alternative sleeve provides valuable protection. To highlight this, we also replicate the above chart from 2000 until 2015, which is shown below.

Performance of SRP vs. SRP + alts excluding Bitcoin (equal weight) at 10%, 15% and 20% alts allocation (2000-15)

Source: Bloomberg, SouthPeak. Performance indexed to $100 as at 5 Jan 2000.

The performance between the standalone SRP and the SRP + alternatives portfolios starts diverging during and after the GFC, which is again driven by equities uncorrelated protection of South Peak during the shock, strong returns of gold following the shock and a steady return from SG trend. The below chart shows the performance of the three alternative assets during that time.

Performance of gold, SG Trend and SouthPeak (2000-15)

Source: Bloomberg, SouthPeak. Performance indexed to $100 as at 5 Jan 2000[?].

Taken together, these results reinforce the point made in the article. While the non-Bitcoin alternatives sleeve does not dominate long-run returns, it consistently improves portfolio behaviour in the environments that matter most to portfolio performance – deep equity drawdowns, inflationary episodes, and periods where bonds fail to provide their expected cushion. That is the diversification benefit that the Alternative Diversifiers™ sleeve is designed to deliver. Bitcoin amplifies both the return and the regime coverage of the alternatives allocation, but the structural case for a multi-asset alternatives sleeve does not depend on Bitcoin alone.

____________________________________________________________________________________________________

1 Our legal eagle doesn’t like this gratuitous use of the “™” but has decided not to object so long as we are stubbornly consistent in its use.

2 See Important information below: any advice in this document is general in nature only.

3 Past performance is not a reliable indicator of future performance. See “Risks, caveats and governance” and “Important information”, both below.

4 The SG Trend Index calculates the net daily rate of return for a pool of trend following based hedge fund managers (equal-weighted and reconstituted annually). Bloomberg: NEIXCTAT Index (Source). Societe Generale entities are not responsible for any use of the SG Trend Index, including as a benchmark.

5 SouthPeak’s Alternative Alpha strategy consists of a ‘protection’ component, which uses long volatility instruments such as put options, and aims to profit when equity markets fall sharply, and a ‘carry’ component which trades volatility-related derivatives aiming to profit in benign market conditions.

6 M3 is the broadest measure of money in the economy: it includes cash, bank deposits and large savings pools held by both individuals and institutions that can be converted into spending power relatively easily.

All third-party brands, indices and trademarks mentioned are property of their respective owners. Their mention in this article is for illustrative purposes: it does not constitute an endorsement of any product, service or strategy.

Important information

® North and MyNorth are trademarks registered to NMMT.

The information on this page has been provided by NMMT Limited ABN 42 058 835 573, AFSL 234653 (NMMT). It contains general advice only, does not take account of your client’s personal objectives, financial situation or needs, and a client should consider whether this information is appropriate for them before making any decisions. It’s important your client consider their circumstances and read the relevant product disclosure statement (PDS), investor directed portfolio guide (IDPS Guide) and target market determination (TMD), available from northonline.com.au or by contacting the North Service Centre on 1800 667 841, before deciding what’s right for them.

MyNorth Investment and North Investment are operated by NMMT. MyNorth Investment Guarantee is issued by National Mutual Funds Management Limited ABN 32 006 787 720, AFSL 234652 (NMFM). MyNorth Super and Pension (including MyNorth Lifetime), MyNorth Super and Pension Guarantee and North Super and Pension are issued by N.M. Superannuation Proprietary Limited (ABN 31 008 428 322, AFSL 234654 (NM Super) as trustee of the Wealth Personal Superannuation and Pension Fund (the Fund) ABN 92 381 911 598. NMMT issues the interests in and is the responsible entity for MyNorth Managed Portfolios. All managed portfolios may not be available across all products on the North platform. All of the products above are referred to collectively as MyNorth Products. The information on this page is provided only for the use of advisers, it is not intended for clients. This page provides a brief overview of some of the benefits of investing in MyNorth Products. The adviser remains responsible for any advice/services they provide to clients including making their own inquiries and ensuring that the advice/services are appropriate and in accordance with all legal requirements.

You can read the Financial Services Guide online for more information, including the fees and benefits that companies related to NMMT, N.M. Superannuation Proprietary Limited ABN 31 008 428 322, AFSL 234654 (N.M. Super) and their representatives may receive in relation to products and services provided.

North and MyNorth are trademarks registered to NMMT.

All information on this website is subject to change without notice.

This article is for professional adviser use only and mustn’t be distributed to or made available to retail clients. It contains general advice only and doesn’t consider a person’s personal goals, financial situation or needs. A person should consider whether this information is appropriate for them before making any decisions. It’s important a person considers their circumstances and reads the relevant product disclosure statement and/or investor directed portfolio services guide, available from NMMT at northonline.com.au or by calling 1800 667 841, before deciding what’s right for them. You can read the NMMT Financial Services Guide online for more information, including the fees and benefits that AMP companies and their representatives may receive in relation to products and services provided. You can also ask us for a hard copy.

Past performance is not a reliable indicator of future performance.

This article includes forecasts, statements and estimates in relation to future matters, many of which are based on subjective judgements and/or proprietary internal modelling. No representation is made that such statements or estimates will prove correct. The reader should be aware that forward-looking statements are predictive in character and may be affected by inaccurate assumptions and/or by known or unknown risks and uncertainties. Results ultimately achieved may differ materially from forecast results. No independent third party has reviewed the reasonableness of any such forward-looking statements or the assumptions on which those forecasts are based.

The performance results in this article are hypothetical back test results for a model portfolio. They do not reflect the performance of actual investments. The back-tested results were achieved by means of the retroactive application of a model that was designed with the benefit of hindsight. This cannot reflect all of the complexities of actual investing and there are many material factors that would have affected actual results, including those relating to the markets in general, the impact of fees and expenses, liquidity activity and other factors, any or all of which may have adversely affected actual performance.

A number of the statements are based on information and research published by others. We have not confirmed, and do not warrant, the accuracy or completeness of that third-party information or research.

All third-party brands, indices and trademarks mentioned are property of their respective owners. Their mention in this article is for illustrative purposes: it does not constitute an endorsement of any product, service or strategy.